Microsoftâ Solutions:

The European Insurance Industry

![]()

Microsoftâ Solutions:

The European Insurance Industry

![]()

In the digital age, the ability to manage information has become a prerequisite for success – and indeed this applies to the insurance industry. Insurers must react more quickly to customer needs, bring products to market with greater speed, and respond more completely to changing business conditions. To meet these demands, many organisations are developing a digital nervous system (DNS) — a new approach that allows them to build on existing technology to create highly efficient, integrated systems that collect, manage, organise, and disseminate information throughout an enterprise.

A digital nervous system helps institutions get the right information to the right people at the right time, provides them with the tools to analyse that information, and gives them the power to act on their conclusions with speed. It also eliminates the piles of forms and layers of approvals that can make even simple day-to-day tasks time consuming and expensive.

Simply put, a digital nervous system is the culmination of the next stage of the information revolution. It is a powerful way to marshal the benefits of digital technologies to meet the challenges of the digital economy - and it is becoming increasingly essential. Institutions that embrace this approach are using technology to ensure that employees can collect the knowledge that resides within the organisation to respond with creativity and speed to changes in the marketplace.

During the last decade, the business landscape has undergone a fundamental transformation. The proliferation of personal computers linked together in enterprise networks and the rise of the internet have played a significant role in the creation of a true world-wide economy in which information travels around the globe in the blink of an eye.

With customers using the web to find out almost instantly who has the best product at the best price, mass production is giving way in many industries to mass customisation. Meanwhile, changes in the economic climate of one region can affect economies around the world.

In the face of these changes, speed has become essential for survival, and the ability to adapt quickly to shifting demands in the marketplace has become a prerequisite for success.

"In a Darwinian business world," says Microsoft Chairman, Bill Gates, "the quality of an organisation’s nervous system helps determine its ability to sense change and quickly respond, thus determining whether it dies, survives, or thrives."

The term digital nervous system implies that this new form of enterprise information management will enable organisations to behave more like biological organisms. This is apt and important.

In biological organisms, the nervous system automatically controls the basic systems - respiratory, circulatory, digestive - that make life possible. It also receives sensory stimuli, transmits them to the brain, and instantly triggers a response. In higher organisms, the nervous system makes it possible to think and plan with foresight and creativity.

To meet the demands of the digital economy, organisations must be able to behave more like organisms. This will give them better reflexes for reacting to stimuli, a more efficient metabolism for managing daily operations, and a sharper mind for guiding plans and actions more intelligently.

But what are the specific business and technology issues that act as stimuli for a digital nervous system within the insurance arena?

And how can technology be applied to create an efficient metabolism for the insurance market?

This white paper focuses in detail on the individual technology components and applications which provide the sensory channels required within a digital nervous system.

"Virtually everything in business today is an undifferentiated commodity except how a company manages its information. How you manage information determines whether you win or lose."

“…the

quality of an organisation’s nervous system helps determine its ability to

sense change and quickly respond, thus determining whether it dies, survives,

or thrives.”

Bill

Gates

Microsoft Chairman

PART I: BUSINESS ISSUES................................................................................................ 1

Introduction....................................................................................................................... 1

Overview of the European insurance market...................................................................... 2

A single European market?......................................................................................... 2

Expansion, globalisation and diversification............................................................ 4

The need for value creation......................................................................................... 5

Developing underwriting expertise............................................................................. 6

Product development and diversification.......................................................................... 9

Product diversification in non-life insurance......................................................... 10

Insurance distribution - the changing mix.............................................................. 12

The impact of bancassurance.................................................................................. 13

The growth of direct insurance................................................................................. 13

The response of the broker channel...................................................................... 15

Multi-channel management..................................................................................... 15

The need for asset management expertise.......................................................... 16

Insurance Technology...................................................................................................... 18

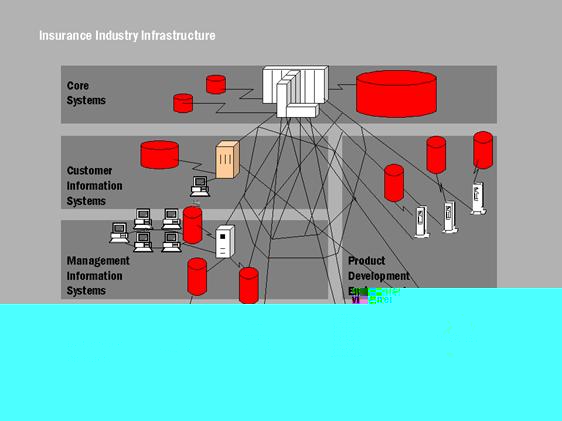

Core systems............................................................................................................... 18

Customer Information Systems............................................................................... 19

Management Information Systems......................................................................... 19

Product development environments...................................................................... 20

Distribution channel technologies........................................................................... 20

Summary and conclusions............................................................................................... 21

PART II: TECHNOLOGY SOLUTIONS................................................................................. 23

Introduction..................................................................................................................... 23

Core Technologies........................................................................................................... 24

Microsoft Windows DNA............................................................................................ 24

Microsoft Windows operating system family......................................................... 25

Component based architecture............................................................................... 26

Component services.................................................................................................. 26

Legacy integration....................................................................................................... 27

Presentation of data................................................................................................... 27

COM+: Enabling the future of Windows DNA....................................................... 28

COM+ services............................................................................................................ 29

Existing services – unification of COM and MTS.................................................. 29

New COM+ services................................................................................................... 30

Turning data into information - datawarehousing support................................. 30

Security.......................................................................................................................... 31

High volume, reliable processing power................................................................. 32

Microsoft Windows 2000 Server............................................................................. 33

Management............................................................................................................... 33

Applications platform................................................................................................. 34

Networking and communications........................................................................... 34

Information sharing and publishing......................................................................... 35

Technology summary....................................................................................................... 36

The next step............................................................................................................... 36

European insurance has traditionally been a static, heavily regulated and domestically focused industry. Throughout most of this century, it has evolved slowly and gradually broadened its scope and size as insurance products cover increasingly diverse areas of risk.

However, it is now witnessing unprecedented change as a result of deregulation, globalisation and the entrance of new players from both European markets and the US.

The industry has been

forced to respond to external pressures, which have transformed a once

stable and predictable sector into an uncertain, fluctuating, but more

dynamic and responsive industry.

The industry has been forced to respond to external

pressures, which have transformed a once stable and predictable sector into an

uncertain, fluctuating, but more dynamic and responsive industry. This is

prompting a wave of consolidation in an attempt to survive through obtaining

greater geographical scope and financial mass, thereby providing more value to

customers and shareholders. Insurers are realising that they can no longer merely

offer a broad product range to a wide customer base. It has become imperative

to increase client management skills to retain customers in the medium to

longer-term.

Overview of the European insurance market

The European market is

suffering from overcapacity, even though there are high concentration

levels in many individual countries.

The European market is suffering from overcapacity,

even though there are high concentration levels in many individual countries.

Countries such as Norway and Finland had 88.6% and 73.4% of their markets

controlled by the top five companies in 1997, and although this concentration

ratio was much lower in larger countries, the average unweighted ratio for

Europe was 54.8%.

However, while insurers are often strong in their domestic markets, few are dominant at the European level. Europe’s largest insurer, Allianz, only obtained 6.5% of total European gross written premiums (GWP) in 1997, followed by AXA-UAP with 5.9%. The other major players only achieved no more than 3% of this market.

Europe is full of small,

domestically focused insurers whose survival had been due to the regulatory

conditions which limited competition.

At a European level the market is very fragmented.

Europe is full of small, domestically focused insurers whose survival had been

due to the regulatory conditions which limited competition. Consequentially,

the deregulation process which has gradually spread across Europe this decade

has been encouraging greater competition, consolidation, and the growth of

pan-European insurance. However, due to the growth of new entrants into the

market, the total number of insurers has only declined slightly in the last

five years, despite high merger and acquisition activity.

Despite consolidation in this sector, the industry still suffers from over-capacity. This is particularly evident in non-life insurance where underwriting results have become increasingly volatile and margins have been consistently low. While the UK has been the most extreme market in this respect, France and Italy also have had poor results in recent years. The effect of deregulation in Germany will continue the trend.

A key instigator of the

state of flux in the European insurance industry has been the impact of the

EU.

A key instigator of the state of flux in the European

insurance industry has been the impact of the EU. The introduction of the Third

Life and Non-Life EU directives has allowed home control of foreign

subsidiaries, facilitating the current drive for consolidation. More

importantly, it has encouraged the deregulation process by allowing companies

to be monitored at a group rather than individual product level. Insurers in

countries such as Germany, Italy and Switzerland are now regulated by solvency

conditions as opposed to individual prices, policy terms and conditions,

creating greater freedom and agility in creating new products and prices.

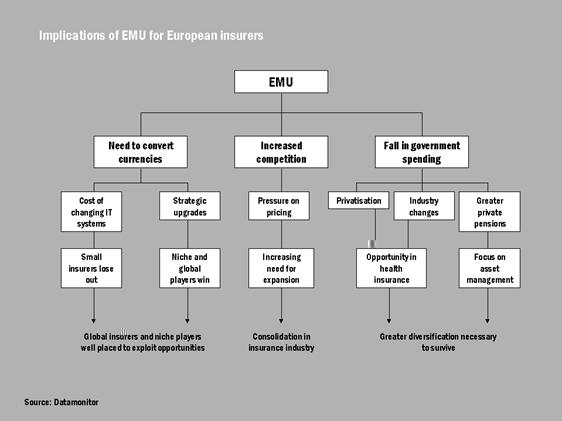

The next major impact from the EU on this industry will be from EMU. Since January, exchange rates in 11 of the EU countries have been fixed to the Ecu, with this currency replacing all of these national currencies by mid-2002. Additionally, those EU countries outside EMU look increasingly likely to join in the near future, with the British government recently announcing preparations to enter as early as 2004.

EMU will have major implications for the insurance industry. In the short term, these will be concentrated on quick fix IT effects as core systems will need converting to deal with dual currencies and meet the new reporting requirements. Additionally, impacts will be felt in the asset management area of insurance as national specific capital constraints are effectively removed. This will lead to further concentration in this sector and heighten the growing requirement for greater funds as size allows lower volatility of investment returns.

In the longer term EMU

will have more strategic effects, encouraging insurers to think on a

pan-European scale in terms of their customers and products.

In the longer term EMU will have more strategic

effects, encouraging insurers to think on a pan-European scale in terms of

their customers and products. This is likely to increase cross-border activity

and accelerate the consolidation process as the larger players acquire smaller

foreign players to establish themselves in non-domestic markets.

Competitive pressures should also intensify as price transparency between member states increases. However, this effect should not be overestimated as prices will still be heavily affected by differing fiscal regimes, combined with regulatory and legal differences. Its greatest impact will therefore be concentrated on corporate customers who operate on a European or larger scale and can take advantage of differing prices across Europe, particularly with the removal of exchange rate risk.

Expansion, globalisation and diversification

The insurance industry

has developed a need for scale which is seen as necessary to survive in an

industry where the numbers of players is decreasing.

EMU will be a driver for European expansion, though

insurers have already been attempting to increase the scale of their reach both

in terms of their geographical presence and through the breadth of their

offerings. The insurance industry has developed a need for scale which is seen

as necessary to survive in an industry where the numbers of players is

decreasing.

The desire for size is partly justified in terms of business logic. The financial services industry as a whole is being affected by globalisation with globally orientated customers increasingly demanding financial services providers which are able to offer a comparable world-wide service. However, few insurers have truly global coverage and this reason does not currently provide sufficient advantage to justify this desire for size. For many, this has been prompted more by the expansion of many US insurers into Europe, as companies (such as AIG) seek more lucrative markets outside the US.

This desire for size is also based upon the stability mass allows by reducing volatility of results (potentially!). The current surge in competition has increased this volatility by accentuating price pressures. Greater geographical reach and diversification across different markets allows more stable results through spreading risk. This has become necessary as stable results have become a prerequisite in Europe’s fickle capital markets for obtaining more consistent valuations, allowing higher future access to capital.

Increased competition has

raised the costs of acquiring new customers and insurers have realised that

cross-selling new products to existing ones is often a more effective

method of increasing revenues and margins.

This drive for geographical reach has been combined

with diversification into new markets. Increased competition has raised the

costs of acquiring new customers and insurers have realised that cross-selling

new products to existing customers is often a more effective method of

increasing revenues and margins. This has occurred across insurance product

lines, with non-life insurers moving into life insurance and vice versa. Many

recent mergers (such as Royal and SunAlliance, CGU plc) have had this reasoning

behind them. The extension of their customer bases presents them with the

opportunity to cross-sell existing products to these newly acquired customers.

Viewing the huge success

banks have had entering into the insurance market, insurers have started to

offer banking products, attempting to leverage their asset and risk

management skills and utilise their direct channel experience.

Additionally, insurers are diversifying outside their traditional

sectors, following the convergence trends within the financial services

industry. Viewing the huge success banks have had entering into the insurance

market, insurers have started to offer banking products, attempting to leverage

their asset and risk management skills and utilise their direct channel

experience. This has been most prevalent in the UK, with insurers such as

Prudential and Scottish Widows starting up their own banking operations. In

Europe, this has predominantly occurred through the formation of alliances and

mergers to create “one-stop-shop” financial supermarkets (a driver behind the

merger of Credit Suisse and Winterthur in 1997).

It is not enough to bring

together two disparate groups and expect economies of scale. The two units

must have complementary factors, and additionally must be easily integrated

from the point of view of IT, customers and distribution.

The desire for growth has for some insurers become an

end in itself. The wave of consolidation has driven some insurers to embark on

expansion programmes which are not necessarily strategically sound. It is not

enough to bring together two disparate groups and expect economies of scale.

The two units must have complementary factors, and additionally must be easily

integrated from the point of view of IT, customers and distribution.

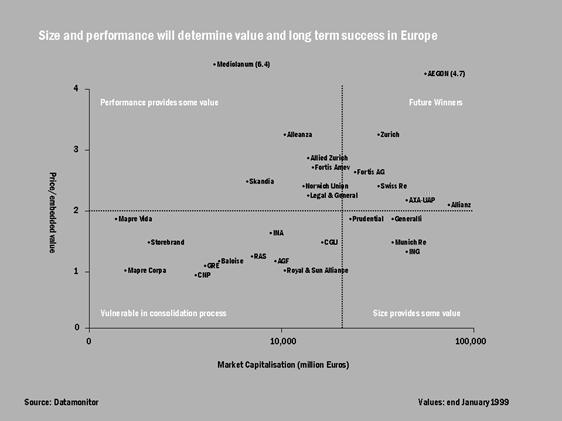

Insurers must be able to provide performance to create value for both customers and shareholders. This is not necessarily achieved by offering a broad product range to a wide customer base. Attempting to derive value through diversification and expansion, rather than through consolidation and niche development, does not account for marked differences between insurers’ business strengths.

A single-minded pursuit of growth overlooks the need to ensure strong returns to shareholders (policyholders in the case of mutuals) via increases in earnings and thus higher dividend payments, rather than aiming for pure maximisation of market share. It is not necessarily the case that an increase in market share will lead to increased profits. Indeed, in many cases acquisition costs can substantially outweigh likely future returns.

Insurers will rarely be

able to add value by expanding outside their core business through

diversification unless they are able to export expertise upon having

reached critical mass in their core business.

Insurers will rarely be able to add value by expanding

outside their core business through diversification unless they are able to

export expertise upon having reached critical mass in their core business.

However, some insurers, such as Generalli, have been able to add genuine value

by building a European position in their sector, as a means to combat

unfavourable economic or claims conditions.

Overall success will be

determined by factors such as strength in domestic markets, combined with a

highly focused business strategy and the ability to excel in the core

insurance competencies of risk management and customer segmentation.

The conditions for creating value will therefore depend

on both size and performance. Overall success will be determined by factors

such as strength in domestic markets, combined with a highly focused business

strategy and the ability to excel in the core insurance competencies of risk

management and customer segmentation. However, actuarial skills alone are not

sufficient for survival as companies must develop expertise in investment, marketing,

customer retention and segmentation, as well as product distribution.

On top of this, insurers must have the ability to aggressively control costs. Rapid restructuring, better expense management through IT implementation and reduction in labour costs are paramount in this process. Norwich Union in the UK, for example, has recently implemented a consistent IT strategy across the whole company. The main aim is to co-ordinate investment management, fund management, pension funds, life insurance and mutual funds using a combination of data warehousing and Intranet technology.

As a result, it is possible to define the areas in which insurers must not only be competent, but also able to outperform competitors. It is only by addressing these components that insurers can truly add value to their clients. In insurance, these areas are:

· developing underwriting sophistication;

· product development and diversification;

· management of distribution systems;

· investment management expertise;

· ability to deal with the IT and strategic issues of EMU.

Developing underwriting expertise

In general insurance, a

key success factor is the ability to control claims. This is achieved by

the development of strong risk management techniques to accurately evaluate

risk and effectively segment customer groups.

In general insurance, a key success factor is the

ability to control claims. This is achieved by the development of strong risk

management techniques to accurately evaluate risk and effectively segment

customer groups. The importance of these abilities has increased due to the

evolution of more volatile underwriting cycles which has and is causing

fluctuations in results and consequently profitability. As mentioned,

maintaining a steady level of returns is essential for improving shareholder

value, which is necessary for gaining future access to capital.

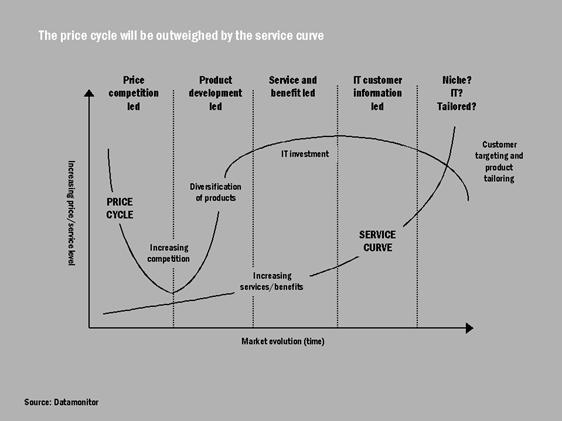

European insurance markets can be understood in terms of the underwriting cycle. As insurance develops in a market, competitors begin to underwrite a greater variety of risks which causes claims to rise. As a result, profitability declines, resulting in some players exiting the market. As competition declines, profitability increases as insurers increase premiums to regain previous losses, thus markets become more attractive and capital and investment increase. Hence insurers are once again forced to lower premiums and accept more risky clients. As a result, claims rise, forcing the cycle to begin once more. Underwriting cycles are more severe in the UK and the Netherlands since these are the most deregulated markets and are also broker‑dominated.

In Europe, while each market in underwriting terms is out of phase with the other markets, it is generally the case that all European insurers have faced tough market conditions caused by over-capacity in recent years. This is leading to low levels of profitability, particularly in motor insurance where competition has increased through the popularity of low-cost direct distribution.

In the UK, the

long-deregulated reference market, underwriting has been extremely

difficult since 1994 and is likely to remain at a low level in the next few

years.

In the UK, the long-deregulated reference market,

underwriting has been extremely difficult since 1994 and is likely to remain at

a low level in the next few years. The market has a large number of large-scale

suppliers but many of the major players have seen their market shares fall as a

result of low‑cost new entrants, particularly in the teleinsurance market

for motor and property insurance lines.

Indeed, it is the volatility of underwriting results in the market as a whole which makes it difficult to foresee future profitability. This, in turn, has detrimental effects for the balance sheet of insurance companies, causing significant fluctuations in the technical account, and reduces the attractiveness of such companies to shareholders. The main causes of such volatility are the increased freedom to set prices, almost non-existent barriers to entry in the UK, tight accounting regulations which forbid claims equalisation reserves and a traditionally high exposure in the market.

The German market, in

contrast, has been the most stable European market due to strict

regulations governing pricing structures which led to low-intensity

competition.

The German market, in contrast, has been the most

stable European market due to strict regulations governing pricing structures

which led to low-intensity competition. However, following the easing of

barriers to foreign entrants and price deregulation, volatility is expected to

increase, particularly in motor insurance as direct channels play an increasing

role in distribution. These fluctuations, however, are unlikely to be as

pronounced as in the UK due to the ability to smooth results using balance

sheet measures.

France, on the other hand, has had fluctuating underwriting results similar to the UK, although this has been hidden to an extent by balance sheet adjustments to smooth results. This fluctuation has been prompted by deregulation which has reduced concentration levels substantially, with many small companies experiencing high growth in both life and general sectors at the expense of the state-led giants, GAN and AGF. This has been achieved through niche focusing with specialised groups, such as Groupe Athèna and Groupama, profiting from lower loss ratios and the ability to exploit niches through innovative product offerings. Similarly, Italy has been experiencing negative returns in its general sector in recent years, although the trend has been upwards. The once stagnant competition in this market has started to intensify due to removal of regulation regarding minimum prices for policies. This will continue as low-cost direct channels grow in popularity. Unlike Germany and France, many Italian insurers are ill placed to deal with this due to the absence of both sophisticated customer data sets and the IT abilities to develop strong customer segmentation and risk management techniques. Thus it is likely there will be a renewed interest in this market amongst foreign insurers, such as Allianz, which are able to utilise more advanced IT systems to penetrate the profitable segments.

As discussed, increased freedom in Europe has increased competition considerably, primarily through the entrance of direct distribution channels which reduce overheads and therefore expense ratios. As a result, prices in commoditised insurance lines such as motor and property will decline in the short‑term. This has been seen in the UK where deregulation occurred earlier than in the rest of Europe. This reduction in prices is a short-term solution for insurers who have not developed sufficient expertise to underwrite risk selectively. Indeed, the resulting decline in profitability which is occurring is driving much of the consolidation taking place in UK non‑life insurance.

As pricing continues to

become more competitive in both life and non-life insurance sectors across

Europe, successful companies will become better risk selectors,

establishing niche customer groups.

As pricing continues to become more competitive in both

life and non-life insurance sectors across Europe, successful companies will

become better risk selectors, establishing niche customer groups. Or, if the

group has sufficient global reach, it will implement measures to reduce

expenses through better distribution and diversification into other financial

services sectors, such as asset management.

Product development and diversification

As the underwriting

environment in almost all European insurance markets deteriorates, it has

become increasingly important for competitors to develop tailored products

and services as a means to retain customers.

As the underwriting environment in almost all European

insurance markets deteriorates, it has become increasingly important for

competitors to develop tailored products and services as a means to retain

customers. This is leading to diversification into new business areas and is

also causing insurers and banks to develop more complex and sophisticated

vehicles, particularly in the life insurance sector. Likewise, in non‑life

insurance, increased service and additional product features are being used to

retain customers as well as attract those of rival competitors.

The maturity reached in many financial services markets, particularly in non-life insurance, is forcing competitors to capture market share from each other in order to achieve revenue growth. However, as price is still the key factor affecting customer decision, insurers are having to offer increased services and product ranges in an attempt to distinguish themselves and maintain market share.

In life insurance,

product development has become increasingly essential due to the high

success banks have had in moving into this sector.

In life insurance, product development has become

increasingly essential due to the high success banks have had in moving into

this sector. This has been based upon the natural synergies between traditional

bank deposits and insurance based savings plans and the cost advantages

obtained from using branch networks for distribution.

This success has been based chiefly around the distribution of simple life insurance products, in order to minimise the selling effort required by bank branch staff. European bancassurers have been forced to spend significant proportions of their budget on training staff in order to familiarise them with insurance products.

It has therefore been essential to minimise further confusion which would augment training costs substantially. Moreover, complex, tailored products would require individual experts in each branch and make these ventures even more costly.

Traditional life insurers therefore have the opportunity to counter the threat imposed by bancassurers by offering tailored products, which are more complex and sophisticated, based upon their stronger underwriting expertise and trained sales forces.

For example, a key area of growth in this area in recent years has been that of unit-linked policies, particularly in the more deregulated countries such as the UK and Netherlands where there has been a strong run in the equity market. In contrast to traditional with-profit policies, offering a guaranteed return with a bonus, unit-linked policies offer a potentially higher, but uncertain return. In this case the insurer makes money from commission charged, instead on the difference between interest received and returns given to policyholders. This offers a lower, but less volatile, source of income as the customer accepts a greater proportion of the policy risk.

Product development is

still heavily dependent on tax incentives, led predominately by the fiscal

status of each European market. Insurers therefore have a strong interest

to base their products around these incentives, in order to market the

higher returns to policyholders.

However, product development is still heavily dependent

on tax incentives, led predominately by the fiscal status of each European

market. Most European countries offer some form of tax incentive, mainly to

encourage savings for old age as governments start to worry about the

demographic shift. Insurers therefore have a strong interest to base their

products around these incentives, in order to market the higher returns to

policyholders.

Thus the UK, with life assurance premiums relief removed in 1984, has moved more strongly towards the unit-linked policies, particularly with the tax incentives around PEP products. In contrast, France gives up to 25% of the life insurance premium price as tax deductible, which has been a strong factor behind the success of bancassurance as banks have packaged life insurance with saving vehicles previously offered to customers.

However, despite a strong effect of tax incentives on product development and as a consequence cross-country activity, innovative product development is now realising new opportunities, even in traditionally the most heavily regulated markets. In Germany, for example, Scottish Amicable International launched a Plan for Life (a unit-linked whole of life protection plan with critical illness and savings plan modules) in October 1995. The product is distributed through networks of independent intermediaries as it is felt that they offer the best access to the chosen customer target group, with local competitors too slow to respond. Indeed, another foreign-owned company, AXA Leben, was the first to respond with a new product of its own, revamping a critical illness product. Product innovation is more important in markets where brokers have traditionally played an important role, for example the UK, Netherlands and Ireland.

The EU could potentially have a large impact on this area, when tax harmonisation reduces the effect of these tax incentives across Europe. In terms of product development, this will move insurers away from a product orientated approach to a customer centric approach. Products will become increasingly tailored to customer requirements, as product development will be based upon meeting the needs of identified customer niches rather than around tax incentives.

Product diversification in non-life insurance

In many European countries, particularly the UK and Netherlands, the success of direct insurance in general insurance has caused strong price competition and placed heavy downward pressure on prices. To provide these low prices, the direct insurers produced simplified and non-specific product offerings to limit costs. Consequently commoditisation of many types of insurance occurred, particularly motor and property insurance.

As consumers have become

more at ease with the concept of direct insurance, they have come to expect

lower prices as standard.

However, as consumers have become more at ease with the

concept of direct insurance, they have come to expect lower prices as standard.

Thus, while price is still the most significant factor affecting the decision

to purchase insurance, the growth of low-cost insurance means price is no

longer a significant source of competitive advantage.

An additional impact of

direct insurance has been to increase customer switching, with customer

churn rates in these commoditised insurance lines rising rapidly in recent

years.

An additional impact of direct insurance has been to

increase customer switching, with customer churn rates in these commoditised

insurance lines rising rapidly in recent years. Churn rates are as high as 34%

for motor insurance in the UK. Strong marketing initiatives enticing the

customer to move to lost-cost insurance have encouraged customers to be more

price sensitive and also reduced customer inertia, due to the ease of acquiring

policies through direct distribution methods.

Insurers are now

attempting to distinguish themselves from their competitors by increasing

their levels of service and offering additional product features.

Therefore, insurers are now attempting to distinguish

themselves from their competitors by increasing their levels of service and

offering additional product features, such as protected no-claims bonuses,

courtesy cars, valet cleaning and the insurer taking the onus for completing

the claims process away from the customer. Customer switching occurs more

frequently after a customer has made a claim and as a consequence, increased

customer satisfaction at the time of claim can reduce customer churn rates.

The key to success now lies in the ability of insurers to distinguish themselves and consequently create a strong brand. Insurers need to be perceived as low cost and high service providers in order to reduce customer switching and make customer acquisition more effective.

The importance of brand

has also become a key factor in the trend of product diversification that

many insurers have embarked upon.

The importance of brand has also become a key factor in

the trend of product diversification that many insurers have embarked upon. The

poor returns suffered in the general insurance sector has encouraged many

insurers to diversify outside their core sectors into life insurance because of

the high returns achieved in recent years.

Many insurers, such as Direct Line, have moved into this market based on brand strength, although because of problems associated with underwriting life policies, this has been achieved by offering very simple life products. Insurers have also circumvented this problem through merger activity to access substantial life customers and underwriting expertise (e.g. CGU or Royal and SunAlliance) or by developing networks for cross selling opportunities (e.g. Credit Suisse and Winterthur).

Insurers have been

attempting to use their brand and customer databases from their core lines

of insurance to cross sell into new product areas.

This movement into life insurance reflects the

underlying diversification trend across all product lines in insurance.

Insurers have realised that it is generally more effective to increase the

profitability of existing customers than it is to acquire new ones which, as

mentioned, requires very competitive prices. Thus insurers have been attempting

to use their brand and customer databases from their core lines of insurance to

cross sell into new product areas.

This allows an insurer to offer a fuller range of products to their customers and so move towards the “one-stop shop” financial supermarket. This is supposed to enable higher customer service as the customer does not need to shop around, but more importantly, diversification allows expansion, growth and a potential increased stability of results which has been deemed vital for increasing shareholder value.

Moving into a new market

will not necessarily improve shareholder value unless expertise can be

exported into the market to provide a competitive advantage.

However, increased breadth needs to be accompanied with

increased depth and insurers must be able to provide a high quality of product

offerings and service across all of their markets. Moving into a new market

will not necessarily improve shareholder value unless expertise can be exported

into the market to provide a competitive advantage. If an insurer is unable to

operate successfully in a new market, value could be destroyed not just because

of the loss of any investment, but also due to brand damage affecting its core

markets.

Insurers must not spread their operations too thinly, both in terms of geographical or sectoral coverage. Low market share in several markets will not add as much value as strong market share in fewer markets. Insurers should have a point of strategic control in either their domestic market or core product market before diversifying or expanding into new markets.

Insurance distribution - the changing mix

The effect of regulation has forced insurers to re-think their strategies with regard to product development and offerings. In turn, this has led to a need to rethink distribution policy.

The introduction of

teleinsurers, banks and retail institutions into the market has caused

traditional insurers to assess the costs and therefore the underlying

profitability of existing channel management.

Traditionally, insurers have used one distribution

channel for all products. Tied‑agents, for examples, have dominated in

France and Germany while brokers have remained important in the UK. However,

the introduction of teleinsurers, banks and retail institutions into the market

has caused traditional insurers to assess the costs and therefore the

underlying profitability of existing channel management. Likewise many have

also wanted to broaden their product range and customer base, for which their

existing distribution structures were not necessarily adequate.

The major changes to distribution have been forced upon insurers rather than based on strategic planning. The first major change has come from the impact of bancassurance, the second from the success of direct insurance. The third impact is a consequence of the first two, that being the need for multi-channel management.

The primary reason for

the success of bancassurance has been the natural synergies between life

insurance products and banks’ traditional saving vehicles.

As mentioned previously, the primary reason for the

success of bancassurance has been the natural synergies between life insurance

products and banks’ traditional saving vehicles. This, combined with the

breadth of bank distribution networks (allowing direct customer contact), the

presence of existing customers and strong brands, has enabled bancassurance to

enjoy rapid growth this decade. The success of bancassurance has been most

notable in Portugal, Spain and France and it is currently developing quickly in

Scandinavia, due to recent favourable taxation for capitalisation products.

Similarly, it is likely to expand rapidly in Greece due to removal of

regulatory constraints and in Switzerland, as UBS and Credit Suisse look to

expand their operations into this area.

In contrast, its penetration has been much lower in the UK. This has been due to the greater importance of the pension market over life insurance. There are less obvious synergies between banks and pension provision than with life insurance. This has been combined with the inability of banks to persuade consumers that life insurance is simple enough to be sold, pre-packaged, over the counter.

Similarly, full non-life bancassurance remains rare in Europe with most banks reluctant to establish comprehensive bancassurance captives in this area, although many offer this insurance as an intermediary. This is due to the small revenue streams generated by personal lines compared to life business, together with the greater investment in IT and training required because of the lower synergies involved. Thus the cost advantage over traditional insurers is much lower.

Additionally, the strong success of direct insurance in this market has made it even more difficult to gain a price advantage. However, selling property insurance as an intermediary based on synergies from mortgages can be extremely profitable. Ironically, banks in the UK are relatively successful property insurance intermediaries, despite the lack of life bancassurance.

The growth of direct insurance

In contrast to the

success of bancassurance in the life insurance sector, direct insurance,

particularly through teleinsurance, continues to experience high growth in

the general insurance sector.

In contrast to the success of bancassurance in the life

insurance sector, direct insurance, particularly through teleinsurance,

continues to experience high growth in the general insurance sector. Like

bancassurance this success has differed across Europe, with highest penetration

rates achieved in Northern Europe, particularly Sweden and the Netherlands,

while take-up has been distinctly low in the Germanic regions.

The introduction of direct selling was led by Centraal Beheer in the Netherlands, which used the telephone as a means to attract customers. Direct Line quickly followed in the UK, as a result of which insurance selling and underwriting became available through this channel. Initially, competitors were able to attract customers by increased brand awareness together with the low-price and ease of delivery which could be offered through the removal of expensive intermediaries.

The greatest impact of

direct insurance has been in commodity type products, such as motor and

property insurance.

The greatest impact of direct insurance has been in

commodity type products, such as motor and property insurance. This is due to

the customers perception of the product as simple and willingness to accept

insurance without consulting an expert. Additionally, direct insurers rely on

the customer contacting them, so the product must be easily identifiable.

The success of direct insurance has been more limited, apart from in the Netherlands and some Scandinavian countries where customers are culturally used to dealing over the telephone. Insurers such as Virgin rely heavily on their brand and reputation for customers to purchase simplified versions of more complex products.

The impact of direct insurance has been much lower in the Germanic and Southern European regions. This limited development is partly cultural, with face-to-face contact being important, but also partly regulatory, such as in Germany where insurers could not set policy prices and thus direct insurers could not undercut. The removal of many of these regulatory constraints in recent years means that strong growth of this channel is expected over the next five years.

While direct insurers are

able to attract customers through lower price points, retention and

maintenance of stable market share is more difficult to establish.

However, while direct insurers are able to attract

customers through lower price points, retention and maintenance of stable

market share is more difficult to establish. As mentioned, the impact of

greater marketing by direct insurers has increased consumer awareness and

reduced customer loyalty to their existing insurer. Thus, high levels of

quality and service, as well as price, are the key factors in retaining

customers over time.

Key conditions for continued success in teleinsurance will therefore be based around risk assessment and pricing control as marketing activities cannot sustain performance in the longer-term without strong underwriting expertise.

The ability to gather and

manage information which enables ongoing development and identification of

customer profiles is the key to future niche operations as a means to manage

risk more successfully.

The ability to gather and manage information which

enables ongoing development and identification of customer profiles is the key

to future niche operations as a means to manage risk more successfully. This

flexibility will provide significant competitive advantage as competition

increases further and pricing structures come under pressure. Examples of such

strategies include AIG, through its subsidiary Landmark Express, targeting

drivers over 50 to reduce risk, and Admiral, which has gathered extensive data

on London, enabling them to set prices accurately and minimise risk

accordingly.

The response of the broker channel

The impact of the success

of both bancassurance and direct insurance has been felt strongest on the

traditional intermediary distribution channels, such as brokers and

tied-agents.

The impact of the success of both bancassurance and

direct insurance has been felt strongest on the traditional intermediary

distribution channels, such as brokers and tied-agents. The adoption of new

technologies allowing more efficient processing and lower administration costs

initially gave these new channels a substantial cost advantage. Additionally,

the smaller size and geographical scope of brokers meant they were unable to

compete in terms of scale with the strong marketing push by the larger direct

insurers or have the customer contact opportunities that branch networks provide.

The rapidly declining

market share has caused consolidation in the broker industry with the

formation of large broker networks with comparable reach to the banks.

However, while these initial advantages enjoyed by

these new channels allowed their consequent high penetration into the insurance

market, the broker market has since responded. The rapidly declining market

share has caused consolidation in the broker industry with the formation of

large broker networks with comparable reach to the banks. Additionally, the

technology gap between brokers and direct insurers has declined as IT costs

have fallen and brokers have been able to adopt new technologies.

As the broker market has responded to the competitive pressures, direct insurers have realised the need to regain links with the intermediary channel. This allows the insurers to market products with increased customer service, due to the face-to-face element provided by the broker channel. For the broker, partnerships can help limit erosion of market share and may allow funding from the insurer for IT systems enabling more efficient processing and EDI link-ups.

However, the broker lays charge to the claim of providing impartial advice and differing levels of commission between insurers could constitute a conflict of interest. Additionally, the benefit of partnerships are limited to life products and the more complex general insurance products, where customers are more willing to pay a premium for more personal advice.

The movement by direct insurers back towards the use of intermediaries and the realisation by most traditional insurers that they need a direct as well as traditional distribution has created a major challenge for insurers. They are now having to deal with customers through several channels and this presents significant challenges in presenting a consistent front to the customer and dealing with pricing issues for each channel.

Multi-channel management

creates a strong business problem as conflict will arise if the same

product is sold to the same customer from different channels.

Multi-channel management creates a strong business

problem as conflict will arise if the same product is sold to the same customer

from different channels. If channels are remunerated independently, they will

effectively be in competition with each other and thus unlikely to co-operate

in the sharing of customer information or cross-selling leads. This will result

in lower customer service and loss of potential sales.

To maximise the benefits

of multiple channels, there needs to be a co-operative strategy between

channels.

These conflicts can be reduced by careful demarcation

of products and customer segments between channels to clearly define and manage

the roles of each channel in the distribution process. However, to maximise the

benefits of multiple channels, there needs to be a co-operative strategy

between channels, in particular salesforces, intermediaries, and direct

channels based on:

· information sharing;

· flexibility;

· creating long-term relationships;

· clear customer segmentation;

· competitive commissions to promote long-term loyalty of intermediaries.

In addition to the business problems, information sharing between channels requires integration of customer databases and technology between channels.

The need for asset management expertise

Competition and deregulation means product development capabilities in the back office are essential. The front office has also been affected, with the use of multiple distribution channels. Similarly, these drivers are causing high growth in middle office activity as customer analysis and risk management become essential for long-term success.

An additional area of insurance that has been affected lies in the investment management element of insurance. This is particularly important in life insurance, where a shift towards equity based products has made obtaining high investment returns essential.

The life insurance market has been growing strongly throughout most of Europe, particularly in the southern countries. This is being driven by demographic pressures, forcing governments to encourage private provision for retirement.

However, this trend has also placed a strong competitive pressure upon life insurers, due to the impact of mutual funds. These are currently only popular in a few European markets such as the UK and France, but high growth is expected across Europe in the next five years, particularly in Sweden and Switzerland due to aggressive marketing from strong players.

Mutual funds offer an

opportunity for life insurers if they can develop unit-linked life

insurance products. However, their growth is also a threat.

Mutual funds offer an opportunity for life insurers if

they can develop unit-linked life insurance products. However, their growth is

also a threat. Many customers use these funds for medium term investments and

their uptake has been high with the younger generation, where the need for life

insurance is not always deemed as urgent.

The demand for these funds is strongly linked to the performance of the equity markets, correlating highly with rapid growth in these markets this decade. Consequently, recent volatility in the global markets may reduce the rate of growth of unit funds. Additionally, lower interest rates and comparisons with the US suggest that the high growth (over 20%) seen in Europe in recent years is not sustainable in the long term.

However, in addition to the threat from traditional fund management operations, banks are also increasing their presence in this arena. This is particularly true for global banking groups such as Deutsche Bank, Zurich and ABN AMRO, as well as smaller institutions like Société Générale who have moved to purchase asset management and investment banking functions.

So far, this greater competition has generally been from domestic players due to regulations around this area of the economy. The UK is the most open economy in this respect with 25% of funds managed by foreign companies in 1998. However, EMU will have a significant impact in this area by eliminating exchange risk and blurring the distinction between foreign and domestic investment. This is likely to lead to a reduction in regulations concerning investment restrictions and an increase in equity diversification across Europe.

Insurers will have to

obtain a critical mass of investment funds, minimising risk through

diversification and cutting transaction costs, thereby increasing returns.

The key effects on the insurance industry will be that

competitive pressures in this field will increase and consequently the need to

produce high and stable returns will grow. As such, insurers will have to

obtain a critical mass of investment funds, minimising risk through

diversification and cutting transaction costs, thereby increasing returns.

It may therefore be beneficial to offer third party asset management facilities to non-insurance clients. This has become increasingly common with the larger European insurers such as AXA-UAP, Winterthur, Zurich and ING, all of which have sufficient funds to gain competitive economies of scale.

In contrast, smaller insurers must decide whether to continue asset management functions in-house or to outsource to a larger player. This will be increasingly common as consolidation in the sector continues and the smaller players become less able to offer competitive returns.

The trend will intensify as US players continue to move into Europe in order to diversify their risk and take advantage of their size and asset management expertise in a deregulating market. Similarly, this is encouraging many of the larger European players, such as AXA-UAP and ING, to move into the US to diversify their risk and also to establish themselves as global players in the financial services industry.

It will be crucial to

develop expertise to manage third party funds and develop expertise in the

equity market where many insurers have previously been restricted due to

regulations.

In the future, consolidation in the industry will occur

and insurance companies must decide whether to outsource their asset management

operations or expand to reach a critical size in terms of funds managed and

geography. To this end it will be crucial to develop expertise to manage third

party funds and develop expertise in the equity market where many insurers have

previously been restricted due to regulations.

The IT infrastructures of

large composite insurers are categorised by the presence of large-scale,

batch oriented, core processing environments.

The IT infrastructures of large composite insurers are

categorised by the presence of large-scale, batch oriented, core processing

environments. Insurers were amongst the first users of mainframe computing when

it was introduced in the 1960s. The shear scale of processing requirements was

an ideal fit for mainframe applications.

Today, these environments remain. In fact, the demand for processing power has increased (policy information must be retained, even when the policy expires. A typical insurer can have 20 million records, of which only 8 million are ‘live’). The predicted death of the mainframe for high volume, transaction based processing has been proved wrong. Hence, the effective use of modern computing technologies in the insurance sector is a complex challenge.

Product support and core

processing systems are the backbone of the established insurer. Legacy

systems remain the biggest IT concern of these companies, which have the

largest asset base of the insurance sector.

Product support and core processing systems are the

backbone of the established insurer. Legacy systems remain the biggest IT

concern of these companies, which have the largest asset base of the insurance

sector. There is interaction in this area with external organisations such as

actuaries and independent claims adjusters. The back office in IT terms is

dominated by batch processing applications used for policy administration and

settlement.

New entrants need

flexible and scalable systems, rather than large, cumbersome applications.

New entrants to the sector do not have the same core

systems issues. New entrants need flexible and scalable systems, rather than

large, cumbersome applications. Core IT systems have, in fact, become a strong

driver for the choice to build separate businesses rather than integrate with

existing applications. Indeed, many new entrants have been driven by the need

for flexible systems.

Insurers are striving to implement ‘customer centric’ business models. The cohesion of the heterogeneous IT environment described above is critical for this to be achieved. Accessing valuable legacy applications is having a profound effect on the use of new technologies. Increasingly, internet technologies are being used for this (the Ohio Casualty Group, for example) which connects its sales force to a series of legacy applications using an internet based layer.

Customer Information

Systems should provide fluidity between product support, customer service

and business development.

In the insurance sector, the use of customer

information is balanced between product support and customer profitability

analysis. Customer Information Systems should provide fluidity between product

support, customer service and business development. To this end, IT systems are

oriented around manipulation and dissemination of information to both the

channel and marketing areas.

With the growing

implementation of independent departmental systems, redundant and

inconsistent data led to inaccurate analyses. The data warehouse solved

this problem by amalgamating data from a wide range of functions.

The development of the data warehouse has enabled

companies to consolidate customer information and use it to improve competitive

advantage. Before the practical application of a data warehouse was possible,

organisations built business decision-making systems designed to assist

specific departments, such as marketing. With the growing implementation of

independent departmental systems, redundant and inconsistent data led to

inaccurate analyses. The data warehouse solved this problem by amalgamating

data from a wide range of functions. This allows collection of more accurate

and complete information.

The insurance sector is particularly suited to the use of data warehouses by virtue of its large customer base and complex product profile. Despite some early problems with implementing data warehouses, as experienced by most sectors, insurers are now having more success.

Client-server databases continue to ship high volumes, primarily to support the roll out of new applications. Insurers have come to rely on such databases for increasingly demanding applications and a growing number of concurrent users. The principal areas of client server database growth are in the middle office, in the regions of Management Information Systems (MIS) and product development environments.

Management Information Systems

Insurers of all sizes are

striving to control channels, so the distribution of information around the

enterprise is critical.

The complexity of distribution channels makes the deployment

of management information systems a critical IT challenge. Insurers of all

sizes are striving to control channels, so the distribution of information

around the enterprise is critical. To meet this challenge a range of

technologies are being employed.

The two types of management information are at a strategic and tactical level. Strategic level information is used for marketing, with data warehousing a key technology. The emerging area of development is at a tactical level, with insurers seeking more control over the operation.

Product development environments

Modern application

development techniques involve the re-use of business objects to help build

applications more quickly.

Rapid time to market has put increased pressure on

product development methodologies in all vertical markets. In the sector, this

demand is exaggerated by the individuality of products. Modern application

development techniques involve the re-use of business objects to help build

applications more quickly. By re-using predefined business logic, insurers can

assemble new, tailored products more rapidly, hence increasing customer

satisfaction and reducing development costs.

A large UK insurer approached application development with its Strategic Build Programme, combining systems for Quotation, Product & Underwriting and Customer Contracting. The core goals of this project were to:

· create new applications within an ‘architectural framework’;

· give business users increased control and flexibility;

· support product and organisational independence;

· reduce development costs and timescales;

· minimise maintenance load and cost;

· produce systems which meet business requirements and provide technical robustness.

Rapid development technologies are particularly popular amongst medium sized composite insurers. Product developers have an intuitive building tool with which they can roll out individual products, while at the same time re-using pre-built business logic.

Distribution channel technologies

Insurers are faced with

the challenge of managing non-tied agents and independent brokers and must

develop IT systems which allow effective product and customer management

through different users.

The distribution channel dynamics of the insurance

sector are very different from those of banking. Insurers are faced with the

challenge of managing non-tied agents and independent brokers and must develop

IT systems which allow effective product and customer management through

different users.

In technology terms, the front office is the best example of a multiple technology environment. Increasingly, front office business strategies have been driven by technology rather than supported by it. Call centre technologies and the internet continue to force fundamental questions about the business strategy of insurance companies.

European insurance is emerging out of a transformation period which will result in substantial consolidation within the industry. This will lead to the polarisation of the industry with the creation of very large pan-European insurers at one end of the scale and small, niche players at the other. Medium sized operations will be squeezed out of the market unless they can create substantial value for their shareholders and customers.

To survive, insurers will have to create value. As discussed, this is not necessarily achieved by offering a broad range of products to a wide customer base. Insurers must focus on their core competencies and expand from positions of strength and strategic control. However, in the long-term, insurers will need to offer both breadth and performance based upon a strong domestic foundation and significant non-domestic positions, combined with expertise in actuarial, risk management and asset management functions.

Successful insurers will

be those who can gain competitive advantage through their IT to improve

their control over costs, customer service and their ability to offer and

cross-sell a broad range of products to a large, but targeted customer

base.

An essential element of value creation will be the

ability to competently manage and utilise the benefits IT offers. Technology

has become an integral part of the insurance process, rather than just a

support factor. Consequently, successful insurers will be those who can gain

competitive advantage through their IT to improve their control over costs,

customer service and their ability to offer and cross-sell a broad range of

products to a large, but targeted customer base.

Microsoft recognises that the insurance industry, like many other parts of the financial services industry, is going through big changes in working practices caused by various factors.

Business and technical decision makers are faced with many choices that will affect both the short and long term profitability of the business. To make these decisions easier, Microsoft has developed a clear strategy.

Microsoft's goal is to

provide the technology platform, Windows, that will enable financial

institutions to develop and deploy solutions in a cost effective and timely

manner.

Microsoft's goal is to provide the technology platform,

Windows, that will enable financial institutions to develop and deploy

solutions in a cost effective and timely manner. Building upon this solid

platform, the vertical line-of-business applications will be provided either

through the IT departments of the financial institutions themselves or through

third party suppliers.

Technology has to address the key needs of the insurance industry:

· to integrate and inter-operate with the core processing systems that exist within insurance companies;

· to manipulate and disseminate vital product information and customer data, to the delivery channels;

· to provide new, innovative solutions to the channels in a time and cost efficient manner, that allows reuse of existing business functionality.

Microsoft has created a framework called Windows Distributed interNet Applications Architecture (DNA) that enables businesses to more easily build new systems that take advantage of the capabilities of the personal computer and the opportunities presented by the internet, whilst integrating with existing systems.

Windows DNA provides an

interoperability framework based on open protocols and published interfaces

that allow customers to extend existing systems with new functionality.

Windows DNA integrates the personal computer standard,

the internet and legacy infrastructures by enabling computers to inter-operate

and co-operate equally well across both corporate and public networks. Windows

DNA provides an interoperability framework based on open protocols and published

interfaces that allow customers to extend existing systems with new

functionality. This same open model provides extensibility ‘hooks’, so third

parties can realise new business opportunities by creating compatible products

that extend the architecture.

The heart of Windows DNA

is the integration of the internet and client/server application

development models through a common object model – the Microsoft Component

Object Model (COM).

Windows DNA applications use a standard set of

Windows-based services that address the requirements of all tiers of modern

distributed applications - user interface and navigation, business processes,

and data storage. The heart of Windows DNA is the integration of the internet

and client/server application development models through a common object model

– the Microsoft Component Object Model (COM). Windows DNA provides a common set

of services that are exposed in a unified way at all tiers of a distributed

application.

By taking advantage of the capabilities in Windows DNA, insurance developers can build entirely new categories of applications, including electronic commerce and other interpersonal and inter-corporate communication applications. Because they are taking advantage of standard implementations of networked services and modern, component-based development methods, developers can deliver these innovative applications much faster and more cost effectively than previously.

Traditionally, insurers and other financial services institutions have built separate IT systems and infrastructures to service the different business opportunities and requirements as and when demand arose. In this environment, an insurer must maintain and administer a number of different client platforms – ranging from simple 3270 based terminals through to an integrated PC environment. Typically these platforms are so different there is little opportunity to share user, administration or development skills across them. If business process analysis shows that certain applications should be deployed at a particular point of contact, it is not possible to do so because each of these platforms is targeted to one particular task. These issues lead to increased operations, development and training costs and an inability to adapt quickly to changing business requirements.

Microsoft Windows operating system family

The Microsoft Windows

operating system family allows financial institutions to choose the most

appropriate hardware platform for the task to be performed.

The Microsoft Windows operating system family –

Microsoft Windows CE, Windows-based Terminals, Microsoft Windows 95/Windows 98

and Windows NT/Windows 2000 – allows financial institutions to choose the most

appropriate hardware platform for the task to be performed. Handheld PCs and

portables can be used to support mobile users. Windows-based Terminals, where

applications and data reside completely on the server, can be used in

task-oriented environments, where manageability and cost of ownership are

paramount. NetPCs offer reduced cost and complexity while maintaining the

choice and flexibility associated with PCs. High-end workstations offer

advanced levels of functionality and flexibility. This highly scaleable and

manageable family of solutions, with a common Windows architecture, allows

financial institutions to maximise the investment they have made in

applications, development skills, help desk systems, technical expertise, and

end user knowledge of the Windows operating system.

Windows CE has proven

itself capable of handling the most demanding 32-bit embedded applications

and brings the full power of the Microsoft 32-bit Windows-based development

tools to the embedded systems designer.

Microsoft Windows CE is a compact, highly efficient and

scaleable operating system that is being used in a wide variety of embedded

products, from hand-held PCs to specialised industrial controllers and consumer

electronic devices. Windows CE has proven itself capable of handling the most

demanding 32-bit embedded applications. Equally important, Windows CE brings

the full power of the Microsoft 32-bit Windows-based development tools to the

embedded systems designer.

One of the primary reasons to choose Windows CE for embedded applications is the widely used Microsoft Win32 Application Programming Interface (API). The Win32 API is at the core of nearly every 32-bit application being written for Windows today, from high-end server products running on the Microsoft Windows NT operating system to the smallest desktop and embedded applications. Using this technology, developers can now create applications which will support mobile users with the same level of application richness found on other hardware platforms.

Within the Windows DNA architecture, all financial services clients are connected to the Windows NT Server via standard IP based protocols. This lowers infrastructure costs, decreases systems administration costs and increases reuse of administration skills, thus lowering training costs.

By rationalising the core messaging protocols used across financial services clients, financial institutions can benefit from the economies of scale by deploying one set of application components to support these core messaging protocols. These components can be reused across the financial services clients. Because of its seamless support for many network protocols, Windows NT Server acts as a gateway to existing systems and the corporate network. This allows financial institutions to preserve existing network investments and migrate to the new standard networking protocols in an evolutionary manner.

Microsoft and its

partners provide many strategies for preserving existing investments in

transaction processing systems.

Microsoft and its partners provide many strategies for

preserving existing investments in transaction processing systems – MVS,

AS/400, Unix – by integrating them into Windows NT Server-based applications.

These include CICS and XA support in Microsoft Transaction Server, Microsoft

Message Queue Server, OLE DB, Data Transformation Services (DTS), simplifying

the process of importing and transforming data from multiple, heterogeneous

sources into Microsoft SQL Server, and DCOM support on non-Microsoft platforms.

The ability to integrate with existing systems together with its support for new technologies such as the internet and intranet and a wide range of high productivity development tools, makes Windows NT a powerful application development platform. Developers can produce new applications which tie together existing systems and extend the reach of those systems more quickly and easily than ever before.

Within the Windows DNA

architecture, applications are built as a series of components. Microsoft’s

Component Object Model (COM) is the backbone used to knit these components

together.

Within the Windows DNA architecture, applications are