Microsoftâ Solutions:

Challenges within European Retail Banking and Financial Markets

![]()

Microsoftâ Solutions:

Challenges within European Retail Banking and Financial Markets

![]()

"Virtually everything in business today is an undifferentiated commodity except how a company manages its information. How you manage information determines whether you win or lose."

“…the

quality of an organisation's nervous system helps determine its ability to

sense change and quickly respond, thus determining whether it dies, survives,

or thrives.”

Bill

Gates

Microsoft Chairman

In the digital age, the ability to manage information has become a prerequisite for success – and indeed this applies to the financial services industry. Financial institutions must react more quickly to customer needs, bring products to market with greater speed, and respond more completely to changing business conditions. To meet these demands, many organisations are developing a 'digital nervous system'- a new approach that allows them to build on existing technology to create highly efficient, integrated systems that collect, manage, organise, and disseminate information throughout an enterprise.

A digital nervous system helps institutions get the right information to the right people at the right time, provides them with the tools to analyse that information, and gives them the power to act on their conclusions with speed. It also eliminates the piles of forms and layers of approvals that can make even simple day-to-day tasks time-consuming and expensive.

Simply put, a digital nervous system is the culmination of the next stage of the information revolution. It is a powerful way to marshal the benefits of digital technologies to meet the challenges of the digital economy - and increasingly it is becoming essential. Institutions which embrace this approach are using technology to ensure that employees can collect the knowledge that resides within the organisation to respond with creativity and speed to changes in the marketplace.

The need for speed

During the last decade, the business landscape has undergone a fundamental transformation. The proliferation of personal computers linked together in enterprise networks and the rise of the Internet have played a major role in the creation of a true worldwide economy, in which information travels around the globe in the blink of an eye.

With customers using the web to find out almost instantly who has the best product at the best price, mass production is giving way in many industries to mass customisation. Meanwhile, changes in the economic climate of one region can affect economies around the world.

In the face of these changes, speed has become an essential ingredient for survival, and the ability to adapt quickly to shifting demands in the marketplace has become a prerequisite for success.

"In a Darwinian business world," says Microsoft Chairman Bill Gates, "the quality of an organisation's nervous system helps determine its ability to sense change and quickly respond, thus determining whether it dies, survives, or thrives."

The term 'digital nervous system' implies that this new form of enterprise information management will enable organisations to behave more like biological organisms. This is apt and important.

In biological organisms, the nervous system automatically controls the basic systems – respiratory, circulatory, digestive – that make life possible. It also receives sensory stimuli, transmits them to the brain, and instantly triggers a response. In higher organisms, the nervous system makes it possible to think and plan with foresight and creativity.

To meet the demands of the digital economy, organisations must be able to behave more like organisms. This will give them better reflexes for reacting to stimuli, a more efficient metabolism for managing daily operations, and a sharper mind for guiding plans and actions more intelligently.

But what are the specific business and technology issues that act as stimuli for a digital nervous system within the financial services arena?

And how can technology be applied to create an efficient metabolism for the retail banking market, the corporate banking market or the financial markets?

This white paper will focus on the range of stimuli that each of these markets has – the business factors as sensory input – and how core Microsoft technologies can be used to provide the platform for a receptive and responsive digital nervous system.

Challenges and responses within European retail banking and financial markets............ 1

Executive summary....................................................................................................... 1

Banking business issues.............................................................................................. 1

Welcome to Euroland................................................................................................... 2

Retail banking.................................................................................................................... 3

Cost reduction................................................................................................................ 3

Product diversification.................................................................................................. 4

The growth of alternative savings products.............................................................. 4

Customer service........................................................................................................... 7

Channels......................................................................................................................... 8

Channel complexity....................................................................................................... 9

Breadth of customer relationship.............................................................................. 9

Customer centricity..................................................................................................... 10

Retail banking business issues - summary............................................................ 11

Corporate banking........................................................................................................... 12

Sizing the SME market............................................................................................... 12

A profitable segment.................................................................................................. 13

Outsourcing cash services......................................................................................... 14

Customer management............................................................................................ 14

Risk management...................................................................................................... 15

Corporate banking business issues - summary.................................................... 15

Financial markets............................................................................................................ 16

Reasons to be cheerful.............................................................................................. 16

Challenges abound..................................................................................................... 17

Mergers and acquisition............................................................................................ 18

Risk management...................................................................................................... 19

Cost reduction............................................................................................................. 20

Financial markets business issues - summary..................................................... 21

Summary of business issues............................................................................................ 22

The technology challenge................................................................................................ 23

The role of technology................................................................................................ 23

Microsoftâ Windowsâ DNA..................................................................................... 24

Microsoftâ Windowsâ operating system family.................................................. 25

Microsoft âWindowsâ 2000 Server...................................................................... 25

Component-based architecture............................................................................... 25

Interoperability............................................................................................................. 25

Security.......................................................................................................................... 25

Scaleability................................................................................................................... 26

Turning data into information................................................................................... 26

High volume, reliable processing power................................................................. 26

Overall Summary.............................................................................................................. 27

Challenges and responses within European retail banking and financial markets

As we approach the millennium, financial institutions are faced with a dilemma. The age of electronic commerce has opened up new ways to reach the customer, new services to offer, and the potential to understand the customer – institutional or personal - as never before. Amidst this background of change, institutions are examining the relationship with their customers, continuing to strive to improve their margins and to increase returns on their equity.

Technology should be an

enabler for financial institutions, assisting them to exploit new opportunities

to the full, not holding them back and restricting their ability to act

swiftly.

Technology should be an enabler for financial institutions, assisting them to exploit new opportunities to the full, not holding them back and restricting their ability to act swiftly. To this end, they need a systems architecture that gives them the flexibility to interface easily with legacy databases and transaction systems hence protecting existing investments, while still being able to make use of emerging technologies.

The year 2000 and the single European currency are just two issues placing an enormous burden on the resources of any organisation. This is compounded by increased banking regulation and the need to be compliant within strict timeframes. The technological revolution within the IT industry is inexorable, giving institutions the ability to rapidly develop new banking products and enter new markets.

The current European banking market is vast, complex, idiosyncratic and national. It, and its institutions, have developed over the years into an industry employing millions, central to the overall economic development of the continent.

As we reach a new

millennium, the politicians of Europe have created a challenge to the

banking industry which is probably greater than anything it has faced

before - Euroland.

As we reach a new millennium, the politicians of Europe

have created a challenge to the banking industry which is probably greater than

anything it has faced before - Euroland. Not since the Roman empire has so much

of Europe accepted the same legal tender and the same central financial control

over economic policy.

Without a proper

appreciation of the business issues facing the banking sector, IT is at

best a blunt instrument.

The implications for the banking industry must now be

considered. Central to these issues and challenges is the role of technology.

Typically accounting for 12% of banking operating costs, technology enables an

institution to operate and serve customers across the continent effectively and

speedily. Without a proper appreciation of the business issues facing the

banking sector, IT is at best a blunt instrument.

The following pages outline Microsoft's views on the key business issues that face Europe. Starting with a brief introduction to Euroland, the next sections explore the business issues and challenges of Euroland in retail banking, corporate banking and financial markets.

January 1999 marked the beginning of a new stage of market development for financial institutions in Europe. At present, 11 countries have adopted the Euro as an official currency. By the end of 2002, it is planned that national currencies will cease to have legal tender status in Euroland.

The total cost of

conversion for financial institutions is estimated at around $15bn, with

around half of the cost to be spent on IT systems.

The total cost of conversion for financial institutions is estimated at around $15bn, with around half of the cost to be spent on IT systems (source, Datamonitor). The cost and implications of Y2K in addition to this have been the focus of much activity and attention.

However, the creation (and probable expansion) of Euroland will also influence a range of business dynamics that will have enormous strategic implications for Europe's financial services industries. Whilst few of these dynamics are completely new, EMU heightens and quickens their impact.

EMU creates a market with

the size and potential of the US market in many areas of banking services. Areas such as consumer

lending, deposit taking and credit cards offer strong Euroland

opportunities. Other areas, where local regulation, taxation and the need

for strong local distribution are high, are less immediately attractive.

On the retail banking side, the prospects for

pan-national products are increased. Areas such as consumer lending, deposit

taking and credit cards offer strong Euroland opportunities. Other areas, where

local regulation, taxation and the need for strong local distribution are high,

are less immediately attractive. Pensions and similar products fall in this

category.

On the wholesale side, Euroland presents significant threats to many traditional areas of business. Swathes of profitable business, such as foreign exchange, corporate deposits, money markets and government bond trading will be reduced. In addition, increasing competition will shave margins in many 'commodity' areas of business such as corporate lending.

However, Euroland will play a part in driving new areas of business. The European municipal and corporate bond market should prosper in a larger, more liquid environment. The larger market should also spur equity-related services and merger and acquisition activity will continue to be buoyant.

Fundamentally, EMU creates a market with the size and potential of the US market in many areas of banking services. In many areas, the scale and scope of operations will be critical and this is scale on a European (or global), not national, basis.

There are three core business drivers which have an impact on European retail banking:

· Cost reduction;

· Product diversification;

· Customer service.

Cost reduction is a challenge in most industries. However, for retail banks, the margin spread between borrowing and lending, the core driver of profitability, is on a cyclical decline as new entrants compete on price (either as lenders or borrowers) and old fashioned relationships with customers are eroded.

Banks are looking to

reduce overall cost to serve, or to find additional revenue streams to

better use existing staff and infrastructures.

Banks are looking to reduce overall cost to serve, or to find additional revenue streams to better use existing staff and infrastructures.

Consolidation is, at one level, a reaction to cost pressures. While other factors have fuelled recent merger and acquisition (M&A) activity, including disintermediation, revenue synergies, political desires to become 'national champions' and EMU, cost reduction remains the main reason. Given that IT costs typically represent 12% of a retail bank's operating costs, they are commonly targeted as a key area for reduction (source Datamonitor).

Merging or acquiring a

large domestic competitor remains one of the most attractive options

available to retail banks. Speculation surrounding the future of even the

largest European banks has arisen.

Merging or acquiring a large domestic competitor remains one of the most attractive options available to retail banks as shown by recent activity, including Société Generale and Crédit du Nord in France, Bank Austria and Creditanstalt in Austria and Ambrovento and Cariplo in Italy. This activity has placed growing pressure on other domestic players to seek partners and there has been increasing speculation surrounding the future of even the largest European banks.

For banks in the smaller, more consolidated markets, such as the Benelux countries and Scandinavia, the trend has been increasingly towards cross-border M&A, for example Merita/Nordbanken and ING/BBL. As the significance of borders between some of the smaller European markets continues to decrease, the definition of what constitutes a domestic banking market is changing. However, the poor post-merger performances of some banks has fuelled scepticism as to the potential benefits of such mergers, given the lack of obvious cost and revenue synergies. Despite this, a number of Europe's largest retail banks have openly expressed a desire to seek cross-border partners and in the wake of EMU this trend is set to continue.

Another key area of cost

reduction is through the outsourcing of different functions.

Another key area of cost reduction is through

the outsourcing of different functions. Banks are re-evaluating what is and

what is not a core function and are seeking to use third-party vendors to

manage an increasing variety of IT and business processes in order to free up

capital for more strategic projects. In Europe, the greatest advances in

outsourcing so far have taken place in Italy where intense cost pressures have

fuelled some of the largest outsourcing deals in the banking industry, such as

the $1.5bn deal announced between EDS and Banca di Roma. M&A activity has

until recently been restricted by legislation, prohibiting the reduction of

branch numbers and staff levels, thus forcing banks to seek alternative

measures of cost reduction. The trend witnessed in Italy can be expected to be

mirrored in other European countries and the range of functions outsourced will

also continue to increase.

In a recent European survey of over 200 banks, conducted by market analysts Datamonitor, leading business decision makers were asked which key areas they were looking to reduce costs in.

Administration staff and

distribution channels appear to be the key areas targeted for cost

reduction over the coming years.

Results showed administration staff and distribution channels (predominantly branch costs) to be the key areas targeted for cost reduction over the coming years. In addition, further reductions in processing costs, still the main area for outsourcing, are expected, combined with minor reductions in customer-facing staff.

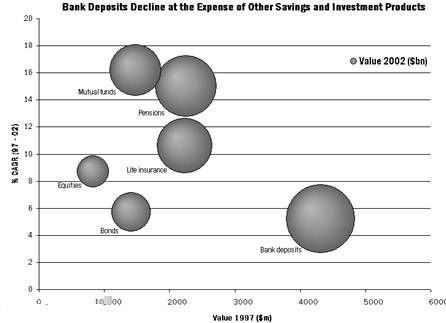

The growth of alternative savings products

Driven by increasing

consumer sophistication and favourable tax benefits, the growth of

non-deposit savings vehicles, such as mutual funds, life insurance and

equities has been dramatic.

One of the most visible areas of change in European

retail banking has been the revolution in personal-sector savings. Driven by

increasing consumer sophistication and favourable tax benefits, the growth of

non-deposit savings vehicles, such as mutual funds, life insurance and equities

has been dramatic. But the core of retail banks' business - the retail deposit

– has suffered at the expense of this growth.

The growth of long-term

savings products, most noticeably mutual funds and life insurance, is

likely to continue.

The growth of long-term savings products, most

noticeably mutual funds and life insurance, is likely to continue as:

· Across Europe, the value of state pensions has diminished in real terms and governments have made it clear that individuals must take responsibility for their own long-term financial requirements;

· Despite recent uncertainty in the financial markets, the long-term widespread gains in European stock markets have boosted the attractiveness of equity-related holdings;

· EMU has moved interest rates down to very low levels in many countries. Whilst the precise objectives of the European Central Bank may change over time, it is unlikely that high nominal interest rates will occur in Euroland in the future. Euroland's low rates will probably put downward pressure on other countries that border the region.

Source: Datamonitor

In response to the threat

of credit disintermediation, retail banks are transforming their offerings

to include many or all of those products, which are shrinking the value of

their retail deposits.

The fact that retail deposits represent a diminishing

proportion of the savings market, does not, however, indicate that the central

role of retail deposits in banking product portfolios will disappear. In

absolute terms, levels of compound growth over the next five years will remain

at around five per cent. But retail banks will require increased flexibility in

terms of product offerings and competitive rates to attract high volumes of

funds. At the same time, costs must be managed down as margin pressure

intensifies in Euroland.

In response to the threat of credit disintermediation, retail banks are transforming their offerings to include many or all of those products, which are shrinking the value of their retail deposits. Banks have developed or acquired asset and fund management expertise and broadened their product base on the life-insurance side, through acquisitions, co-operation agreements and greenfield operations.

In many countries, banks are major suppliers of these products. As insurers battle with the difficulties of EMU and Y2K, banks will seek to exploit their weakness and continue to gain share.

At the same time, Euroland offers opportunities to develop pan-European offerings and customer bases in certain product areas.

There are three key factors which dictate the suitability of offering cross-border banking products:

· Regulatory environments;

· Taxation;

· The suitability of the product for remote distribution.

Direct equity and bond

investments, offer potential for cross-border sales. For many savings and

investment products, such as life insurance and pensions, domestic

differences in regulation and taxation mean the cross-border provision of

such products is unlikely in the short-term.

For many savings and investment products, such as life

insurance and pensions, domestic differences in regulation and taxation mean

the cross-border provision of such products is unlikely in the short-term.

Further harmonisation of the European markets will be required for this to

become feasible.

Direct equity and bond investments, however, offer potential for cross-border sales. Mutual funds, despite certain local tax and regulation difficulties also offer opportunities, particularly as remote distribution is a viable option for sophisticated customers.

In the area of mortgage

provision, while little exists in the way of regulatory barriers, tax

issues would represent a greater potential barrier given that, in most

national markets, tax relief exists for the mortgage holder. From the banks'

perspective, success in the provision of cross-border deposit accounts will

be largely dictated by their cost base (and therefore their ability to

offer superior interest rates) and strength of brand.

Other savings products such as traditional retail

deposits are not subject to such regulatory complications. The single currency

will in theory, give the consumer the freedom to chose whichever country he or

she wants to save in, particularly with the growth of remote channels. From the

banks' perspective, success in the provision of cross-border deposit accounts

will be largely dictated by their cost base (and therefore their ability to

offer superior interest rates) and strength of brand.

In the area of mortgage provision, while little exists in the way of regulatory barriers, tax issues would represent a greater potential barrier given that, in most national markets, tax relief exists for the mortgage holder. The problem that would arise would be the uncertainty of whether or not the holder would be able to claim such relief if the mortgage was purchased in another country. Furthermore, the 'localised' nature of a mortgage product coupled with the requirement on behalf of the lender to have knowledge of local housing market conditions (in order to segment and price risk), would further restrict the potential for cross-border provision.

On the other hand, personal loans would not face the same legal or fiscal challenges. Central to the success of a bank aiming to offer such a product would be the ability to deliver a lower price (interest rate) than domestic competitors, and the possession of sophisticated risk management techniques.

As well as cross-border

sales of existing products, new products for pan-Euroland use will

increase. International by

definition, credit card issuers are anticipating a migration of customers

from non-card payments owing to the potential for confusion during the

transition period.

Despite the development of international payments

systems, debit cards remain largely domestic in use and issuance. Although

international use will increase alongside developments in payment systems, it

is unlikely that EMU will stimulate rapid cross border use. Credit cards,

however, are another case. International by definition, credit card issuers are

anticipating a migration of customers from non-card payments (i.e. cash and

cheques) owing to the potential for confusion during the transition period.

As well as cross-border sales of existing products, new products for pan-Euroland use will increase. These will be designed to meet the needs of customers with financial arrangements that span different countries and regulatory regimes (working in one country, owning property in another, with investments in a third, for example).

The euro, apart from seeing the emergence of cross-border provision and therefore increased competition from outside national borders, will also spur the development of new products. European retail banking is poised to become even more complex.

Customer service can be considered along a number of dimensions:

· Improving distribution and service channels for the customer;

· Managing the customer in a multiple channel environment;

· Deciding on the breadth of the customer relationship;

· Integrating the above into a customer-centric focus.

Distribution channels

have and will continue to be one of the key strategic issues facing retail

banks.

Channels

Distribution channels have and will continue to be one of the key strategic issues facing retail banks. Banks are re-inventing the role of the branch - no longer viewed as a cost centre and increasingly viewed as a sales and 'relationship building' centre. Following forecasts of terminal decline, the value of the branch, particularly to serve small business customers and to sell more complex 'allfinanz' products is widely recognised.

The telephone is now

perceived as a near fundamental component of a bank's distribution channel

strategy in many European countries.

The telephone is now perceived as a near fundamental component of a bank's distribution channel strategy in many European countries. First introduced in the late 1980s by innovators such as First Direct in the UK and Bankiter in Spain, most large European banks reacted quickly by launching their own 'bolt-on' operations to complement existing services. However, this defensive 'me too' approach, was in some cases poorly conceived and the high set up costs combined with an inability to migrate customers away from branch transactions, meant returns on investment were poor.

Recent strategies have paid far more attention to the financial benefits and risks of launching a telephone service and far greater focus has been paid on ensuring integration with existing channels and architectures. Key developments in the future of telephone banking are likely to be based on:

· Increasing convergence and co-existence with online channels;

· Increasing use for the sale of more complex financial services, such as mortgages, loans and alternative investment products.

Much has been spoken and written about online channels. In some markets, notably Germany and Scandinavia, significant progress has been made. Developing an online presence is seen by some as both fundamental to building customer relationships and as a future source of cost reduction.

Questions still remain as

to the real impact online channels offer to a bank's bottom line.

However, questions still remain as to the real

impact online channels offer to a bank's bottom line. Whilst in some markets,

high levels of penetration have been reached, it is not clear whether banks

have been successful in migrating customers away from more costly channels or

whether they have only succeeded in adding extra transactions to their processing

workloads.

The last couple of years

has also seen the emergence of GSM mobile phones as a distribution channel.

Further channels such as digital TV also increase the breadth of

distribution offerings.

The last couple of years have also seen the

emergence of GSM mobile phones as a distribution channel. Pioneered by banks

such as Bank Austria, Dresdner Bank and Banco Santander, their potential for

performing remote, routine transactions and convenience of use is encouraging

strong growth. Further channels such as digital TV also increase the breadth of

distribution offerings.

Whilst new channels offer high potential in terms of improved service, new customer attraction and, in some cases, cost reduction, there are also problems.

In many cases, new

channels have been developed at arm's length from existing distribution

structures.

In many cases, new channels have been developed at

arm's length from existing distribution structures. This 'silo' effect has

meant that integration between different channels has been poor. Costs have not

been reduced but added to. At the same time, the difficulties of presenting a

common look and feel to the customer and gathering customer data across

different channels remain major issues. Multiple channel management will

continue to be a major headache in the coming years.

Breadth of customer relationship

What share of the customer's wallet should a bank aim for? An ongoing debate is in progress as institutions move towards either broad full relationship offerings or choose to focus on servicing specific customer needs.

The concept of the

financial services supermarket is coming back into fashion as banks look

for opportunities to build fee income, capitalise on new savings vehicles

and amortise fixed branch infrastructure costs.

At the same time, partly

due to new entrants, there are organisations that are focusing on

particular product niches, utilising economies of scale, improved methods,

and channels and management focus to carve out successful businesses.

The concept of the financial services supermarket is

coming back into fashion as banks look for opportunities to build fee income,

capitalise on new savings vehicles and amortise fixed branch infrastructure

costs. The perceived need to control both the marketing and manufacture of

insurance and investment products is again leading to merger activity, most

noticeably in the US with Citicorp and Travellers but also in Europe with

Credit Suisse and Winterthur.

At the same time, partly due to new entrants, there are organisations that are focusing on particular product niches, utilising economies of scale, improved methods, and channels and management focus to carve out successful businesses. Capital One and MBNA are examples of these companies in the credit card market, Schwab is an example in securities.

The financial services 'supermarkets' must gain economies of scope if their strategy is to be justified. Otherwise focused niche specialists will slice away particular areas of business leaving the generalists with poorer and poorer returns. The core method to achieve synergies is through moving from a product to customer centric operation, in which customer relationships are managed to allow cross-selling and more and more sophisticated 'financial management' services are developed.

Whilst cross-selling is

the obvious starting point, the end game for the financial conglomerates

must be to offer integrated financial management services for consumers.

Whilst cross-selling is the obvious starting point (and an area of mixed performance), the end game for the financial conglomerates must be to offer integrated financial management services for consumers. This means offering a seamless and integrated set of offerings which allows the customer to combine the best of deposit, investment and insurance products in a bespoke form. It means having the channel structure to allow this to be done at the client's convenience and ensuring consistency of look, feel and operation across channels. It must also mean reducing unit costs by achieving cost reductions through the breadth of offering and channel support.

The concept of customer

relationship management (CRM) has become one of the most talked about

issues in modern retail financial services.

Traditionally, banks have sought to grow revenues

through expanding their customer base, whether it be through expanding branch

networks, aggressive advertising campaigns or through the acquisition of other

banks. However, the high costs associated with this acquisition process have

led to the realisation that improving the profitability of a bank’s existing

customer base makes a far stronger business case. In order to achieve this,

banks must be able to better manage individual customer relationships.

The concept of customer relationship management (CRM) has become one of the most talked about issues in modern retail financial services. In a recent Datamonitor survey, 57% of all banks questioned stated that CRM was a critical component of future bank strategies.

Despite being a 'blanket' term used to describe a number of business processes and technologies, an effective CRM strategy should enable a bank to:

· Improve levels of profitability, through the ability to measure individual customer profitability, profile 'best' customers and design products to meet their needs;

· Improve levels of customer service through consistent delivery, simplified access and service, and the ability to address individual customer needs in terms of products, channels and pricing.

The major hurdle facing

banks in their quest to develop the king of 'lifelong' value-added

relationships aimed for in CRM strategy is the inability to gain an

integrated view of their customer base.

At the heart of CRM strategy, is the ability of the

bank to access and analyse customer information in order to make informed,

personalised decisions about which products/services it should offer to which

customers through which channels. The major hurdle facing banks in their quest

to develop the king of 'lifelong' value-added relationships aimed for in CRM

strategy is the inability to gain an integrated view of their customer base.

Given the fact that customer information is typically scattered across a number

of separate operational databases and files, this lack of integration is

restricting banks in their ability to cross-sell, develop new products and

design effective marketing campaigns.

Retail banking business issues - summary

Strategic direction for many banks is unclear with proponents of both breadth and focus and arguments for local focus countered by Europe-wide ambitions. At the same time, the rate of growth and importance of new channels such as online banking are uncertain. The take-up and demand for many new products is untested.

In this environment, only a few central tenets can be stated with any degree of certainty:

· Costs must come down. Margin pressure, particularly on traditional commodity businesses, will only increase in Euroland;

· Products must develop to service the changing needs of customers in a world of low interest rates and more liquid capital markets;

· The customer must be central. There is still much to do in moving from product-focused systems. Collection, analysis and use of customer information will be critical.

Corporate banking covers the range of businesses from the smallest enterprises through to the largest multinationals. As the size of an enterprise increases, so do its requirements for more complex financial products and financial management services. However, the larger corporate customers are not necessarily the most profitable. This is because:

· Their sheer size gives them far greater bargaining power than small or mid-market companies;

· They have, by necessity, multiple banking relationships which can be exploited to obtain the best value on a deal-per-deal basis;

· They often have the ability to disintermediate banks by raising capital directly via the financial markets.

The mid-sized corporate

market and the small business sector is, however, an increasing area of

focus for Europe's retail banks given the strong growth in population of

these sectors and the potential for highly profitable relationships.

The mid-sized corporate market and the small business sector is, however, an increasing area of focus for Europe's retail banks given the strong growth in population of these sectors and the potential for highly profitable relationships.

The contribution small to medium sized enterprises (SMEs) make to the European economy is substantial. Accounting for over 99% of all enterprises and approximately 60% of total employment, enterprises with fewer than 500 employees form the heart of the European economy.

Over recent years, there has been a structural shift in the population of the SME component of the European enterprise sector, a trend that is set to continue. This growth can be attributed to a number of factors:

· An increase in the volume of downsizing and subcontracting of larger firms creating greater opportunities for smaller businesses;

· A general structural shift in the economy towards service-based industries which are characterised by small businesses;

· Increases in privatisation and deregulation and a lowering of the barriers to entry for small businesses.

These factors, combined with the general growth in self-employed individuals, have made the SME sector highly attractive to financial institutions and other organisations alike.

For Europe's dominant retail banks, the small to mid-sized business sector is intrinsically profitable for a number of reasons:

· Limited new entrants. Barriers to entry are high (for both non-banks and foreign banks) owing to the necessity for an extensive branch network given the frequency of contact between the SME and banks;

·

SMEs shop around far

less, giving banks greater potential to cross and up-sell other financial

services products.

Loyal customers. SMEs are generally very loyal

customers and levels of switching are low. Relationships typically last in the

order of decades rather than years, enabling banks to develop highly personal

and profitable relationships;

· High penetration levels. Compared to the large enterprise sector where corporate customers typically have up to 10 different banking relationships, on average SMEs have less than two. SMEs shop around far less, giving banks greater potential to cross and up-sell other financial services products.

But the position is not as comfortable as it may seem and there are some threats facing Europe's dominant retail banks, most notably EMU and the potential for asset disintermediation as the larger enterprises seek capital-market financing as opposed to bank lending.

Banks must both increase

revenues per business customer and reduce costs in order to retain market

share and profitability.

Banks must both increase revenues per business customer

and reduce costs in order to retain market share and profitability. In addition

to extending the traditional range of products and services offered to their

business customers, in order to increase revenue per SME, banks are:

· Cross-selling ancillary products such as insurance and property services;

· Offering banking and financial services to employees of their business customers;

· Providing outsourcing services for cash management (such as credit control).

Banks are increasingly

taking on a wider range of cash services for their business customers.

Outsourcing cash services

Banks are increasingly taking on a wider range of cash services for their business customers. These include commodity type services such as cash and cheque clearing, to the more value added services such as risk control, balance management and foreign exchange execution. Corporate customers are increasingly outsourcing the more basic services and opportunities for banks are emerging in the provision of value-added cash services.

In so doing, banks are aiming to exploit their expertise in key areas such as risk management to provide lucrative new revenue streams from their existing customer base.

The development of

corporate Internet banking has lagged in the retail banking sector. The need for banks to

build strong relationships with corporate treasurers and business customers

and provide consistently high levels of service is fundamental to success.

As for the financial services industry as a whole,

customer service and relationship management are becoming increasingly central

for success in the area of corporate banking. The need for banks to build

strong relationships with corporate treasurers and business customers and

provide consistently high levels of service is fundamental to success.

To achieve this, significant developments have taken place in the provision of online banking services, although the vast majority remain proprietary and low in functionality.

The development of corporate Internet banking has lagged in the retail banking sector owing to the perceived risk of performing large-scale corporate banking transactions, the potential for greater price competition and the greater levels of complexity of providing business banking services. While this is expected to change over the next three years, the most significant growth will take place in intranet and extranet based corporate banking applications given the greater levels of security and reliability.

But while the efficiency benefits of online corporate banking for both parties are clear to see, the challenge facing banks is to effectively use the information obtained from this interaction to proactively market and sell other products and services.

The regional nature of

small to mid-sized business banking means the branch remains the most

important point of contact for corporate customers.

The regional nature of small to mid-sized business

banking means the branch remains the most important point of contact for

corporate customers. In a decentralised banking environment, this means a large

proportion of all business customer information is held at a branch or at

regional centre level. Having this information stored at local level is

valuable in terms of better understanding the financial requirements of local businesses

and developing more intimate relationships. However, it is limiting in the

respect that it inhibits the bank from performing wide-scale statistical

analyses of its full customer base, and therefore understanding exposure to

high credit risk customers.

By centralising data

storage, banks are running the risk of losing powerful local information

but are improving the ability to make corporate-wide decisions based on

risk exposure.

In choosing whether to store corporate customer data in a centralised or decentralised location, banks are therefore making important decisions. By centralising data storage, they are running the risk of losing powerful local information but are improving the ability to make corporate-wide decisions based on risk exposure. It is not clear which strategy is necessarily the most advantageous. This is likely to be dependent on the relative importance a bank places on the smaller business segment of its customer base.

Corporate banking business issues - summary

As companies,

particularly in the mid to large corporate sector continue to grow the

proportion of funding derived from capital-market financing, the volume of

'traditional' lending income received by banks will continue to decline.

While corporate banking will continue to remain a

central and profitable component of business for Europe's retail banks,

particularly those targeting the mid-market, there are threats ahead. As

companies, particularly in the mid to large corporate sector continue to grow

the proportion of funding derived from capital-market financing, the volume of

'traditional' lending income received by banks will continue to decline. In

order to overcome these losses, banks will have to:

· Build the fee and service based proportion of their revenues;

· Increase use of electronic interaction with their corporate customers to enhance existing levels of service, reduce costs and offer new products and services;

· Increase the use of customer information systems to enhance risk management techniques and to develop targeted marketing and selling campaigns.

1998 was a roller-coaster year for the financial markets. A bull market was cut short in the middle of the year and high profile bailouts were necessary as the downside of highly leveraged hedging operations became apparent. Yet, by the first days of 1999, the markets had recovered to approach all time highs in many countries. The euro was launched with, initially at least, apparent success, and interest rates continued to be low or in decline in the major world economies.

There are strong

fundamental reasons to be optimistic about the future of financial markets.

With this background, it is a brave pundit who

forecasts what is likely to happen over the next few years. But there are strong

fundamental reasons to be optimistic about the future of financial markets.

These dynamics are outlined below. Then, some of the business issues and

implications are discussed.

There are some basic factors that make financial markets, particularly in Europe, a long-term growth area:

· Asset accumulation is continuing as new capital supply from the baby boomers comes into the market looking for investment opportunities;

· Changes in regulation, sophisticated financial engineering and supply push is allowing investment based products to gain share from traditional savings products in all European markets;

· Increasing numbers of European companies will come to the stock market to seek cheaper capital and exits for owners (especially in Germany and Italy);

· M&A activity will progress in Europe as the euro lends weight to ongoing continental industry restructuring;

· Governments move out of social security provision and ownership of assets.

The euro will make it

more cost effective for companies to raise capital, while the privatisation

of social security provision and government-owned industries will bring

significant equity issues in the future.

Europe (and indeed the rest of the world) is

significantly undercapitalised in comparison with the US. The ratio of total

market capitalisation to GDP in Europe is less than half that of the US. The

euro will make it more cost effective for companies to raise capital, while the

privatisation of social security provision and government-owned industries will

bring significant equity issues in the future. Thus, the capitalisation gap

will close. While Europe may not see US levels of capitalisation, even a 50%

closing of the gap would bring another US$1.5 trillion to market.

The nineties has seen an enormous increase in asset accumulation as the baby boomer generation wealth and saving predisposition took effect. This trend will continue. OECD estimates the amount of new capital supply at around US$6 trillion in the period 1992 - 2002.

Moreover, this savings boost is accompanied by a trend toward more sophisticated investment products and away from the traditional retail deposit.

Despite these positive

drivers, the major investment banks have not performed particularly well in

recent years - either in Europe or the US.

Challenges abound

However, despite these positive drivers, the major investment banks have not performed particularly well in recent years - either in Europe or the US. Despite some good years in the mid-1990s, the long-term trend in ROE for investment banking is on a downward trend since 1980.

A worrying issue facing

the investment institution is the gradual erosion of its core source of

income - commissions accrued from intermediation.

The reasons are:

·

Extra competition from

commercial banks has squeezed the fees that investment banks can charge and

forced up staff costs.

Disintermediation. A worrying issue facing the

investment institution is the gradual erosion of its core source of income -

commissions accrued from intermediation. Investment banks had a pivotal role in

a world of poor communications, scarce information and inefficient capital

markets. Today, information about demand, supply and price of capital moves far

more freely, over increasingly networked computer systems. This makes it easier

for buyers and sellers to find one another and complete the deal without the

involvement of the investment bank.

· Increased competition. Commercial banks have entered the market by building up their own capabilities or, more commonly, by merging with or acquiring an existing investment house. This extra competition has not only squeezed the fees that investment banks can charge. It has also forced up their staff costs as the new entrants compete to hire the best stock analysts and traders. Salaries, bonuses and other staff costs typically make up more than half an investment bank's costs. Despite recent lay-offs, this is unlikely to change in the near future.

· Rising costs. Profit has accrued to employees as salaries have risen. At the same time, investments in infrastructure and IT have increased fixed costs substantially, while many areas of revenues are extremely variable with market conditions. Some European banks have IT spends in excess of $500m a year on their global financial markets operations.

·

The market is

consolidating and the smaller players (the bulge bracket) are not making

much money. Major players, including some of the largest European banks

have reduced operations substantially.

Complexity. There has sometimes been a disconnect

between the activities of short-term, bonus-oriented traders, financial

instruments developers who have conceived ever more complex and confusing

offerings and services, and the ability of bank senior management to

appropriately assess their risk and use of capital. This is partly generational,

partly the sheer complexity of some instruments and partly inadequate

comprehensive risk management information and systems.

· Market concentration. The market is consolidating and the smaller players (the bulge bracket) are not making much money. Major players, including some of the largest European banks have reduced operations substantially.

There is a widespread

belief that big is better and that, in an increasingly competitive market

of squeezed margins, only the greatest and the strongest will survive and

prosper.

The trend of concentration is unlikely to slow.

There is a widespread belief that big is better and that, in an increasingly competitive

market of squeezed margins, only the greatest and the strongest will survive

and prosper. Large size in itself affords an institution the ability to make

larger returns, benefit from economies of scale and exploit a more powerful

bargaining position in the market. However, rapid growth is extremely difficult

to achieve organically, and so consolidation has been a key feature in the

financial markets. There have been numerous large mergers and take-overs in the

industry as institutions strive to control a larger share of the market, build

international capabilities and, in some cases, join with others of their

choosing, before they attract the attentions of a predatory acquirer.

However, mergers and acquisitions bring their own challenges. At a strategic level, there may be a clash of cultures, or a loss of focus. At an operational level, the process of integrating teams, infrastructure and information has proved a significant task. The expected synergies that spur companies to merge have often proved difficult to find after the event, while cost savings from rationalisation are similarly elusive.

The most critical factor

of successful integrations has been the flexibility and interoperability of

each organisation's IT infrastructure.

The most critical factor of successful integrations has

been the flexibility and interoperability of each organisation's IT

infrastructure. Robust, high-speed communications and data handling

infrastructures, crucial within any investment bank, become even more important

when two or more organisations are coming together.

Growth, whether organic or through M&A, may also reflect a strategy of diversification. Revenue from a wide variety of financial activities offers some protection from the vagaries of a fluctuating market. The short-term failures of one instrument are offset by gains in others, and the institution as a whole is cushioned from the more damaging effects of a slump. In addition, banks have proved skilful in exploiting synergies between fund management, trading and venture capital, reducing costs in-house but also appealing to large corporate clients as a one-stop shop. The goal is to be able to provide a range of fully integrated investment banking services in each territory of operation.

Standardised, scaleable

systems offer the opportunity to build or integrate new capabilities

quickly and efficiently. Rapid application

development environments allow institutions to radically reduce the time

and cost of developing the complex software needed to support a new

activity.

In striving to build a multiplicity of investment activities, banks need to exploit all the advantages that technological innovation can provide. Standardised, scaleable systems offer the opportunity to build or integrate new capabilities quickly and efficiently. Rapid application development environments allow institutions to radically reduce the time and cost of developing the complex software needed to support a new activity.

Another implication of merger and acquisition activity is a significant increase in the difficulty in accurately and consistently measuring the risk position of the institution. The advantage of different revenue streams providing a defence against sharp market fluctuations is only attainable if management can gain a global view of all the activities of the institution. The difficulty in this undertaking increases exponentially with the size and diversity of the business.

The lack of a coherent,

up-to-the-minute view of a company's exposure can lead to catastrophic loss

of balance.

Achieving excellence in risk management has become

something of an obsession with many investment houses, and it is easy to see

why. The lack of a coherent, up-to-the-minute view of a company's exposure can

lead to catastrophic loss of balance. The past five years have seen some highly

publicised errors, with concomitant implications for the credibility, and even

the financial viability of the companies in question.

Even with these salutary warnings to focus the mind of every bank, the quality of risk management is still questionable. A survey by market analysts, Datamonitor, revealed that over a third of risk managers within European investment banks accepted that large unauthorised trading could still occur within their organisation, leading to significant losses for the banks. This is not the only danger. As trading floors expand, and instruments grow ever more complex, it is the smaller scale exceeding of limits and individual attempts to recoup losses without management that threaten the integrity of the bank’s position.

The same Datamonitor survey suggested that over 85% of traders believed that numerous small scale unauthorised trades had taken place within their organisation, the majority undetected by management.

This seemingly endemic lack of insight and control of banks over short-term, small-scale unauthorised trading, is unlikely to 'break the bank,' but it has the potential to erode expected profits at an alarming rate. Trading banks have concentrated, in recent years, on improving the sophistication of market models and enhancing analytical capabilities at the desktop. There is now an acknowledged need to concentrate on the integrity, breadth and timeliness of the data that feeds this analysis and to gain a coherent up-to-the-minute view of the institution's position.

Investment houses have in

the past sought to reduce costs by scaling back expansion or

diversification plans. However, pulling out of particular activities, and

retreating back into core markets is a drastic way to reduce costs.

The squeeze on margins means that investment companies

need to reduce costs in order to remain competitive. This problem is

exacerbated when the market takes a downturn, as evidenced by the redundancies

at several institutions at the end of 1998. Investment houses have in the past

sought to reduce costs by scaling back expansion or diversification plans.

However, pulling out of particular activities and retreating back into core

markets is a drastic way to reduce costs. Two of the ways in which costs can

realistically be reduced without reducing revenue generating activities or

plans for expansion are:

· Increasing processing efficiency. Straight-through processing has gained widespread credibility as a means of capturing essential data about a transaction as close to initiation as possible so that all trade and settlement processing can occur automatically. This has the added advantage of making the organisation more transparent - facilitating compliance with tightening regulatory requirements.

· Adopting more cost-efficient infrastructure. Modern IT systems can reduce costs significantly by offering groupware, teleconferencing and document sharing capabilities. This is only the first step. Internet trading, currently held back by concerns over security and regulation, will lead to efficient distribution of institutional research services and price offerings. Virtual exchanges will reduce the importance of physical presence and allow companies to reduce the fixed overheads of site, building and staff.

Costs associated with IT

implementation and maintenance are coming down.

Furthermore, the costs associated with IT implementation and maintenance are coming down. New operating systems, zero administration systems management tools and client/server architectures are reducing the cost of ownership of each desktop, and freeing staff to concentrate on developing applications that will more directly benefit the business.

Financial markets business issues - summary

Future strategies advocated in this market include:

· Get big. Only a relatively few companies have the financial resources to play in the major league of traders. If an oligopolistic environment can be created, over the long-term the major investment houses should be able to generate good returns. M&A will continue;

· Focus on building scale in non-trading areas. Venture capital, investment management and custody services are possibilities;

· Build brands where it matters, particularly on the smaller corporate side. This protects the bank from the commoditisation inherent in lending and borrowing. Big corporations have the bargaining power to reduce prices significantly;

· Build integrated financial management services for mid-tier accounts. As with consumer services, client lock-in (and premium pricing) can be achieved through offering a seamless combination of investment, hedging, foreign exchange and insurance products in a quasi-outsourced fashion.

But certain issues need to be addressed:

· Costs must be reduced or variabilised through more efficient IT investment, outsourcing of certain, primarily back office, operations and reducing the bargaining power of certain employee groups;

· Risk must be managed on a corporate-wide basis with the right information being available to the right people at the right time;

· Analytical capabilities, at the trading desk, must continue to develop as banks compete in more and more sophisticated and complex markets;

· The whole business cycle from analysis, marketing, execution through to settlement must be speeded up to gain competitive advantage and reduce costs.

European banking is entering a new period of opportunities and threats. Euroland brings specific challenges and issues, but primarily it increases the impact of existing business forces and pressures. Whether in retail banking, corporate banking or financial markets, certain key themes will continue to dominate the thinking and strategies of financial institutions:

· The need to provide customer value and therefore profit through new products and services as traditional sources of income dry up;

· The need to contain or reduce costs, including IT costs, as new entrants and aggressive competitors impact the market;

· The need to integrate data rapidly and effectively in order to manage risk and enhance customer relationships.

But as well as

challenges, there are also opportunities. Euroland is a vast economic

space, rivalling the United States in its potential.

Achieving shareholder value will, as always, rest on a lot of determined, unsung hard work by all the employees of the bank. But as well as challenges, there are also opportunities. Euroland is a vast economic space, rivalling the United States in its potential. Undoubtedly some European institutions will develop continent-wide leadership either in mainstream or niche sectors of the banking industry. This is a tremendous prize.

Can today's major

institutions be flexible and nimble enough to respond quickly to market

changes? There is increased

confidence in the Internet as a medium for financial transactions and

information distribution.

Systems are being created and deployed which help

measure and manage risk exposures across multiple products, banks and

currencies. Internet technologies make it easier to communicate with external

customers and enhance internal communication. This gives customers not only ubiquitous

access but alleviates many of the problems and costs associated with software

distribution. The recent de-restriction of the encryption laws from the US has

increased confidence in the Internet as a medium for financial transactions and

information distribution to a client base whose industry and technological

knowledge is rapidly increasing.

Financial institutions find themselves wondering whether they are at a disadvantage to new entrants to the marketplace starting with a clean sheet. It is clear that the competitive advantage will go to those who have the skills and the intelligence to transform this vision into reality. Can today's major institutions be flexible and nimble enough to respond quickly to market changes, increased regulation and to introduce new products fast enough in response to changes in customer and market demands? Established firms have an advantage in terms of their acquired expertise and knowledge of their customers, but when faced with a heritage of disparate systems, it can prove hard to locate and organise that data to full advantage. The proliferation of diverse systems can be expensive to maintain as well as making it hard to take a consolidated, enterprise-wide view of the business. The globalisation of banking institutions highlights this problem.

Many of the business

problems facing financial institutions have a common factor - they demand a

component based, modular IT infrastructure.

Many of the business problems facing financial

institutions have a common factor - they demand a component based, modular IT

infrastructure, to allow easy integration into legacy environments, to allow

the consolidation of distributed data to provide a single client profile, and

to provide the framework into which emerging products can be added in order to

adapt rapidly to changing customer and regulatory requirements. The ability to

re-use the same application components across all business areas reduces a

firm's product development and maintenance costs, as well as significantly

reducing the time-to-market for new products or even entering new markets.

Financial institutions are faced with a difficult set of business challenges as they move towards the millennium. More and more pressure is being placed on their IT departments and IT infrastructures to help meet those challenges.

Business managers are placing many demands on their IT departments. They are demanding new IT systems that service the customer. These new systems must be as flexible as possible to meet the ever increasing demand for new products and to meet the demands of ever stricter regulatory authorities. They are demanding systems that enable the automation of cumbersome and time consuming paper-based business processes.

Business managers are

asking for existing systems to be re-engineered to produce customer rather

than account focused IT systems, to deliver existing services to the Internet

and to allow datamining of customer information.

Business managers are asking for existing

systems to be re-engineered to produce customer rather than account focused IT

systems, to deliver existing services to the Internet and to allow datamining

of customer information. At the same time, many other demands are being placed

on IT departments. They are being asked to lower the cost of development, to

shorten the development life cycle and to reduce the cost of delivering new

systems. They are being asked to reduce the costs of existing infrastructures,

to overcome the problems posed by the Year 2000 in existing systems, and to add

support for the single European currency.

The challenge is to take advantage of the power of the new technologies - the ever increasing performance of low-cost, ubiquitous PC-based devices, the global communications infrastructure provided by the Internet, the decreased development times provided by component based architectures - to service these demands. This must be done without having to write off investments in existing systems or build expensive new distributed computing infrastructures.

Microsoftâ Windowsâ DNA

Microsoft has created a framework called Windows Distributed interNet Applications (DNA) Architecture that allows businesses to more easily build new systems that take advantage of the capabilities of the personal computer and the opportunities presented by the Internet while integrating with existing systems.

The heart of Windows DNA

is the integration of the Internet and client/server application

development models through a common object model - the Microsoftâ

Component Object Model (COM).

Windows DNA integrates the personal computer standard, the Internet and legacy infrastructures by enabling computers to interoperate and cooperate equally well across both corporate and public networks. Windows DNA provides an interoperability framework based on open protocols and published interfaces that allows customers to extend existing systems with new functionality. This same open model provides extensibility 'hooks', so third parties can realise new business opportunities by creating compatible products which extend the architecture.

Windows DNA applications use a standard set of Windows-based services that address the requirements of all tiers of modern distributed applications. The heart of Windows DNA is the integration of the Internet and client/server application development models through a common object model - the Microsoftâ Component Object Model (COM). Windows DNA provides a common set of services that are exposed in a unified way at all tiers of a distributed application.

By taking advantage of the capabilities in Windows DNA, developers can build entirely new categories of applications, and by taking advantage of standard implementations of networked services and modern, component-based development methods, developers can deliver these innovative applications much faster and more cost effectively than previously.

Microsoftâ Windowsâ operating system family

The Microsoft Windows

operating system family allows financial institutions to choose the most

appropriate hardware platform for the task to be performed.

The Microsoft Windows operating system family - Windowsâ CE,

Windows-based Terminals, Windowsâ 95 / Windowsâ 98 and Windows NTâ/ Windowsâ 2000 -

allows financial institutions to choose the most appropriate hardware platform

for the task to be performed.

Microsoft âWindowsâ 2000 Server

Microsoft Windows 2000 Server provides the basis for information technology managers who want to develop architectures for the future while addressing today's computing challenges. Microsoft Windows 2000 operating system will bring advantages in the areas of management, application infrastructure, networking and communications, and information sharing and publishing.

The Microsoft Windows 2000 platform is comprised of Microsoft Windows 2000 Server and Microsoft Windows 2000 Professional. Using both the server and the client versions of the next generation Windows operating systems will allow the building of a computing infrastructure on a lower cost, flexible platform, that can readily adapt to changing needs.

Microsoft Windows CE is a compact, highly efficient and scaleable operating system that is being used in a wide variety of embedded products, from hand-held PCs to specialised industrial controllers and consumer electronic devices. Windows CE has proven itself capable of handling the most demanding 32-bit embedded applications. Equally important, Windows CE brings the full power of the Microsoft 32-bit Windows-based development tools to the embedded systems designer.

In the Windows DNA architecture, applications are built as a series of components. Microsoft's Component Object Model (COM) is the backbone used to knit these components together. The Microsoft Component Object Model (COM) is an accepted standard, and the multitude of programming languages which support this model allow developers to create applications in the environment with which they are most familiar.

Microsoft and its

partners provide many strategies for preserving existing investments in

transaction processing systems.

Microsoft and its partners provide many strategies for

preserving existing investments in transaction processing systems - MVS,

AS/400, Unix - by integrating them into Microsoft Windows NT Server based

applications.

Windows NT Server offers a secure, robust and scaleable platform for demanding, commercial use. Comprehensive and usable security was a major design goal of Windows NT Server - ensuring that security is integrated and comprehensive.

Above and beyond this, Windows NT Server is highly scaleable so that even very large companies can have a manageable total number of servers, reducing security management costs, and making a security audit easier.

Making better business decisions quickly is the key to succeeding in today's competitive financial marketplace. Understandably, financial institutions seeking to improve their decision-making can be overwhelmed by the sheer volume and complexity of data available from their varied operational and production systems. Making this data available to a wide audience of business users is one of the most significant challenges for today's information technology professionals.

Microsoft SQL Server 7.0

offers a great breadth of functionality to support the data warehousing

process.

Microsoft has also been developing a number of products

and facilities such as Microsoftâ SQL Serverä 7.0 that are well

suited to the data warehousing process. Coupled with third party products that

can be integrated using the Microsoft Data Warehousing Framework, customers

have a large selection of interoperable, best-of-breed products from which to

choose for their data warehousing needs. Microsoft SQL Server 7.0 offers a

great breadth of functionality to support the data warehousing process.

High volume, reliable processing power

Within the financial services arena, it is not only necessary to provide systems which can process high volumes of transactions, but also to provide systems which will ensure uninterrupted processing, since the opportunity cost of system downtime is unlimited. Microsoft invested considerable time and expertise in symmetric multiprocessing (SMP) technology for Windows NT Server, allowing it to run on machines with up to 32 processors, meeting the transactional demands of the industry. The technology necessary to achieve genuine, load-balancing, symmetric multiprocessing is intrinsic to all components of Windows NT Server.

Maturing electronic

delivery channels have the potential to deliver better service at lower

cost.

Banks are often faced with a paradox when trying to

increase their profitability at the same time as developing new delivery

channels. However, the maturing electronic delivery channels have the potential

to deliver better service at lower cost. With this in mind, financial

institutions are recognising how a single technology platform and database can

provide the backbone they require in order to compete within the changing

marketplace. In the retail financial services area this may include NetMeeting

and NetShow to interact remotely with their customers in real-time via the

Internet. In the financial markets area, the same consistent technology

backbone can be used to provide information quicker and more rapidly than

before, either internally to improve reporting, or externally to smooth the

trading process via straight-through processing.

Financial institutions have a vision for the future of banking: delivering a flexible and responsive service to the customer whenever and wherever the customer requires it.

This vision needs to be supported by flexible, customer-focused IT systems. These IT systems must take advantage of the power of new technologies without requiring financial institutions to throw away their existing transaction processing systems, and they must cost less time and effort to build than in the past.

Windows Distributed interNet Applications Architecture (DNA) delivers a comprehensive set of services that provide a consistent programming model, a consistent development environment, consistent distributed services and a consistent application model to the desktop and the server. These services are powered by the proven technology in the Windows family of operating systems and the Microsoftâ BackOfficeâ family of applications.

By building to this architecture, financial institutions can more quickly and easily build delivery channel applications which integrate the new technologies with their existing systems to provide more customer service at lower cost than ever before.